Report

Rental stock falls sharply due to deteriorating investment climate

November 20, 2023

Looking for a PDF of this content?

After almost a decade of massive investment in Dutch housing by both domestic and foreign investors, we are now seeing a significant pullback. Of course, this is partly the result of rising interest rates, but the main culprit is the deteriorating investment climate.

In 2015, the then Minister of Housing and Public Service decided to make the investment climate more attractive for (inter)national investors through tax benefits and reducing the role of housing associations. This investment space was eagerly used: no fewer than ten to fifteen thousand new-build homes were added every year. In addition, private investors in particular added a significant number of existing homes to the buy-to-let market. But despite this wave of growth, the housing shortage worsened, partly due to inaccurate projections of migration and household growth, which were underestimated. This has led to surging housing costs, both in the owner-occupied and rental sectors.

As access to affordable housing declined, public outrage grew. Calls to curb rent increases, especially excessive ones, became louder and louder. In recent years, municipalities have responded to this outcry, focusing not just on the most egregious rent hikes, but mostly on ensuring the availability of affordable housing across the board, including for vital professions. In recent years, they introduced the following measures, among others, which have been largely successful:

- buy-back protections and self-occupancy obligations;

- rental price agreements for long-term letting of affordable rental properties;

- rental price indexations;

- mandatory allocation of housing to certain income or occupational groups;

- obligations for property developers to commit to affordable new-build programmes*.

Still, the central government felt that additional action was needed, and is currently working on instruments such as a tougher tax regime and additional rent regulations (the Affordable Rent Act). In doing so, it is pursuing the same goals as municipalities, namely to guarantee the affordability of rental housing and to eliminate excessive rents. Our previous study on the proposed rent regulations showed that the impact on landlords could cause the measures to backfire. They could, for instance, cause landlords to change their investment strategy and sell their properties, which would lead to a decline in rental housing stock. Now that the introduction of the intended rental regulation on 1 July 2024 is approaching, the question is whether the first effects are already visible on the rental housing market. How are the plans affecting both the availability and affordability of rental housing?

Our previous study on the proposed rent regulations showed that the impact on landlords could cause the measures to backfire. They could, for instance, cause landlords to change their investment strategy and sell their properties, which would lead to a decline in rental housing stock. Now that the introduction of the intended rental regulation on 1 July 2024 is approaching, the question is whether the first effects are already visible on the rental housing market. How are the plans affecting both the availability and affordability of rental housing?

Every three months, the existing rental stock in the G20 decreases by more than 1,300 homes – and this number is increasing

An analysis of cadastre data – including registered deliveries of homes – shows no growth so far in the number of sales of individual properties by landlords to owner-occupiers. In fact, since the first transfer tax increase, sales by - for the most part private landlords and professional investors that sell off rental properties to the owner-occupied market - have fallen by around 25% in the 20 largest Dutch municipalities. This is offset by the fact that landlords are buying increasingly fewer homes from owner-occupiers.

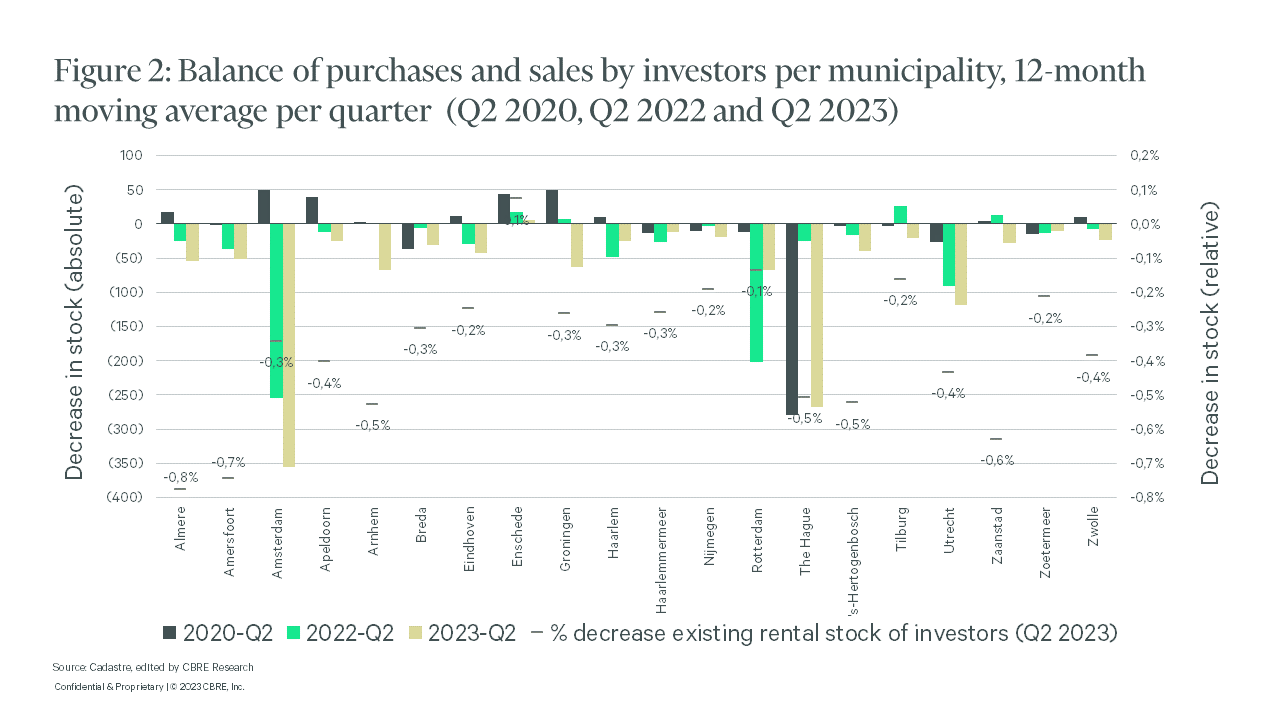

Due to the combination of these developments, the rental housing stock has been steadily shrinking since the beginning of 2021, a development that seems to have gained momentum in the past year. In the second quarter of this year, for instance, the number of homes sold to owner-occupiers in the 20 largest municipalities exceeded the number of homes purchased from this group by 1,316. This means that the rental housing stock in the second quarter of 2023 fell by 0.3% in these municipalities.

It is clear that the private buy-to-let market is shrinking sharply. Initially, this was due to the transfer tax increase and the introduction of buyout protection, but a lot of the current decline can be attributed to the announced adjustments to Box 3 and the proposed regulations for the mid-rent segment. Simply put, the existing rental housing stock is contracting, despite the fact that expanding the stock would contribute to a more moderate development of market rents and a better balance between supply and demand.

If we zoom in to the municipal level, we see that many large cities have a withdrawal rate of 0.4%. The connection may be relatively weak, but there does appear to be a correlation between the likely impact the proposed regulations will have on net rent levels on the one hand, and the extent to which landlords are selling off their properties on the owner-occupied market.

At present, the impact of selling off rental properties appears to be greatest in Almere, Amersfoort, and Zaanstad. This may be due to higher mutation rates in these cities – when a tenant moves out, the landlord is presented with a natural opportunity to sell their property in the owner-occupied market.

Because rent levels vary from city to city, it is also possible that some investors’ rental portfolios – depending on their composition – will be hit harder by the new rent regulations than others. Partly for this reason, it is important to understand, looking at specific housing characteristics, which part of the rental housing stock is most likely to fall into the regulated segment and would thus be subject to significant rent adjustments following mutation once the Affordable Rent Act is passed.

According to our analysis, large parts of the rental housing stock in Zaanstad, Arnhem, Den Bosch, Almere and Amersfoort, among other municipalities, will be hardest hit. In Arnhem in particular, however, the impact on net rent levels will be smaller than in cities such as Amsterdam and Utrecht. In Amsterdam, rent levels will almost be halved, which would have a substantial impact on investors’ net returns. In fact, direct gross yields for a large number of rental properties in Amsterdam are set to drop well below current mortgage rates, in many cases leaving no financial headroom for maintenance, improvements or sustainability renovations.

Table 1: Current and future rental opportunity – e.g. Amsterdam city centre; 60 sq. m.; energy label C [1]

|

Example |

Current situation |

Future situation |

|

Purchase price 2022 |

€ 510,750 |

€ 510,750 |

|

Rent |

€ 1,700 |

€ 947 |

|

Total rental income |

€ 20,400 |

€ 11,364 |

|

Rental income gross yield |

4.0% |

2.2% |

Source: CBRE Research

As the impact on yield is highly dependent on the location of the rental property, it is legitimate to group municipalities according to the expected level of impact (high, medium or low) in the further analysis.

Table 2 clusters the 20 largest Dutch municipalities based on expected impact. This is estimated on the basis of expected rental impact, composition of the rental housing stock and the expected mutation rate. This is generally higher for smaller apartments in the big cities than for single-family homes in peripheral areas, which are less affected by this change in the law. With everything we know now, the following impact levels seem realistic for these municipalities:

Table 2: Expected impact level in the 20 largest Dutch municipalities

|

Impact level |

Municipalities |

|

High impact |

Almere, Amsterdam, The Hague, Den Bosch, Rotterdam, Utrecht, Zaandam |

|

Medium impact |

Amersfoort, Eindhoven, Nijmegen, Haarlem, Groningen, Zwolle |

|

Low impact |

Apeldoorn, Arnhem, Breda, Enschede, Haarlemmermeer, Tilburg, Zoetermeer |

Source: CBRE Research

[1] Average purchase price in 2022 of one 60 sq. m. home in the centre of Amsterdam

Phasing of the impact

How soon the impact of selling off rental properties becomes measurable (or more measurable) depends on when the Affordable Rent Act is expected to come into force, as well as on the average mutation rate. Based on recent conversations we have had with landlords, it appears that we are still in a preliminary phase in terms of the large-scale selling off rental properties, with no negative impact on net rent levels yet. On the contrary, with rent levels rising faster, mutations can often result in higher rents. Nonetheless, many landlords are still exploring the possibility of selling off their rental properties on the owner-occupied market.

Figure 4: Impact phases

Preliminary phase: little selling off, but first effects are already noticeable

In the preliminary phase, we see that investors start to invest primarily outside the Dutch housing market. This partly explains the sharp drop in the number of existing homes purchased by investors in the 20 largest Dutch municipalities, from an average of 6,441 in 2020 per quarter to 2,898 by 2023 – a 55% decrease. This represents a more than €1 billion decline in quarterly investment in the housing market compared to three years earlier.

Although investors are increasingly investing in foreign housing markets and other real estate sectors, such as logistics and retail, their interest is mainly shifting to other asset classes, such as stocks, government bonds and savings deposits. In theory, these should now generate better returns than residential investments. This is largely due to the increased transfer tax and the potential impact of regulations on net rent levels of residential real estate.

Despite this shift in investment allocations, we have yet to see any major changes in the strategies of small private landlords, partly because – notwithstanding fiscal changes – they are not yet significantly affected by declining net rent levels due to the announced regulations. As a result, many investors do not feel an urgent need to adjust their strategy. This makes sense, as they have yet to feel the impact of the expected regulations on their direct and indirect returns.

It should be noted here, however, that a large proportion of private landlords use temporary leases. While they can currently still offer a two-year lease to new tenants, this will no longer be possible from 1 July 2024. The risk of further regulation is also high, given the programmes of the parties running in the upcoming general election. The likelihood of increasing costs for landlords, with no exit option, makes it very unattractive to offer tenants a permanent contract. This means that the rate of rental properties being sold off on the owner-occupied market is expected to rise in the first two years after the abolition of temporary contracts.

In the current preliminary phase, we are already seeing a drop in the available supply for tenants. On the one hand, the available supply is shrinking, as investors are buying fewer owner-occupied homes to put on the rental market. On the other hand, tenants’ willingness to move is declining as a direct result of the scarcity in the rental market. Because of higher mortgage rates, they are usually unable to move to an owner-occupied home, but cannot move to another rental home either due to the smaller – and therefore increasingly expensive – supply. We spoke to all institutional investors currently active in the Dutch market. This revealed that the mutation rates in almost all their portfolios are down by 1 to 3 percentage points year-on-year.

Our analyses further showed that this effect is occurring mainly in the rental housing segments and municipalities that will be affected more strongly by the proposed regulations for the mid-rent segment. A conclusive causal relationship cannot yet be established, but it is certainly notable that the available supply is declining the most in municipalities where the impact is likely to be greatest. In addition, the available supply is only decreasing sharply in the part of the unregulated segment that will eventually be regulated.

First and second phases: selling off of rental properties accelerates, mutation rates drop sharply

Once the Affordable Rent Act comes into force and introduces regulations for the mid-rent segment, the investment outlook changes, which will set off a chain reaction. If a tenant moves out, the next tenant’s net rent will be lower. As a result, direct yield will drop by 28% to 47%, depending on the location. This decline in rental income will lead to substantially lower property valuations, which in turn will have a strong negative impact on indirect returns. One possible consequence is that mortgage lenders will charge higher interest rates or ask for additional repayments.

Finally, the proposed fiscal measures – further restrictions on interest deductions, the abolition of so-called FBIs (fiscal investment institutions) and higher tax rates – will also have a negative impact. All in all, this will put additional pressure on operating yields, making it more attractive for landlords to sell their rental properties in the owner-occupied market. In fact, this will most likely be their only option.

Many landlords will choose to sell off their properties once their current tenants give notice. As a result, the speed at which the rental housing stock can be expected to shrink will depend heavily on the mutation rate. Foreign regulatory initiatives and domestic differences in mutation rates between social housing and the unregulated sector also play a role. Taking all this into account, the mutation rate for homes that will be regulated once the Affordable Rent Act comes into force can be expected to fall to a level just above the average mutation rate for social housing in the coming years. Initially, however, there will be a brief uptick following the abolition of temporary contracts.

CBRE estimates that the mutation rate will drop below 10%, down from a current range between 15% and 17% for more expensive homes in major cities[2]. This will have two main consequences. On the one hand, the available supply in the newly regulated sector will be decimated, causing waiting lists similar to those for social housing. On the other hand, the declining mutation rate will lead to a lower impact of selling off rental properties.

As a result, it will take at least another 20 years – possibly even considerably longer – before all homes that would fall under the new regulations following a mutation are sold on the private owner-occupied housing market. This implies a limited impact on pricing within this market. Only at the local level can there occasionally be a limited downward effect on prices in the owner-occupied market, mostly in the first few years.

As some landlords are keen to speed up this process, some investors will choose to sell to their current tenants. We know from experience that, in smaller apartments in cities, this method leads to accelerated levels of sales to owner-occupiers in approximately 15% of cases. The rate of selling off rental properties to the owner-occupied market can be projected based on:

- the developments set out above;

- the structure of individual municipalities’ rental stock;

- our conversations with key landlords, large and small.

Based on our analysis, we expect the existing Dutch rental housing stock (owned by investors) to decrease by around 13% in the years ahead, solely as a result of the introduction of the Affordable Rent Act. This means that, in the longer term, the investor-owned rental housing stock will shrink from 751,200 to 651,400 homes. This projected decrease does not take into account the possible addition of new-build homes, although the limited number of building permits currently being issued makes it highly unlikely that the existing shortage will be resolved.

Thus, the new regulations will eventually remove some 100,000 existing rental properties from the rental market. This comes on top of the impact of the proposed fiscal changes on the selling off of rental properties, the effect of which has not been included in this study.

Clearly, the rental stock is shrinking disproportionately in the larger cities, where the impact on net rent levels will be strongest. This is all the more worrying as it is precisely in these markets that demand for rental housing is highest, exacerbating market tightness. Moreover, this will seriously hamstring labour mobility, making these cities less attractive to students and expats.

Overall, the stock of investor-owned rental housing in the major cities (most of which already falls into the social housing segment) is set to fall by 20%. Nationwide, the projected drop is 13%. However, the rental housing segment that will be impacted most strongly comprises 32% of the total stock. As a result, a large proportion of rental housing in the Netherlands will be lost to the owner-occupied market.

In municipalities where the impact is expected to be average, we foresee a decline in investor-owned rental stock of around 14%. In a majority of municipalities, which collectively represent about half (52%) of the total rental stock, the impact will be limited to a decrease of 3%. The main reason why the decline in rental stock will be relatively minor in these municipalities is that the impact on net rent levels will be very limited – or even non-existent. This should allow most landlords in these municipalities to continue letting their properties.

[2] This applies to more expensive homes in major cities. For homes with lower rents (in the unregulated sector), mutation rates are already closer to 10%.Deteriorating investment climate and interest rate hikes expected to create second wave of sales to the owner-occupied market

Besides the selling off of rental properties as a direct result of the regulatory changes, we foresee that the deteriorating investment climate and interest rate hikes will lead to a second wave of rental properties’ sales on the owner-occupied market.

Many institutional investors reassess their housing portfolio on an annual basis to ensure continued alignment with their increasingly ambitious sustainability goals and any adjustments in their investment strategies. This means that each year 5,000 to 25,000 existing rental properties are bought and sold in the residential investment market as housing complexes change hands. In recent years, however, we have seen a clear change in the profile of the investors buying these existing housing complexes.

Our analyses show that most existing complexes have historically been sold back to investors with a buy-to-let strategy. On average, only 7% of these portfolios came into the hands of investors who bought the complexes as part of a strategy to sell off to the owner-occupied market. Foreign pension funds in particular bought these kinds of portfolios with the aim of making them more sustainable and letting them on a long-term basis. Whereas foreign entrants normally adopt a strategy of buying up several existing residential portfolios, we are now seeing more restraint among this group. The causes for this are, once again, the deteriorating investment climate, the significantly increased transfer tax and increasing regulatory pressure.

The number of foreign entrants to the Dutch market has declined over the past two years. This is despite a number of positive attributes of the Dutch housing market, which they highly value, such as a relatively strong economy and demographics. Foreign pension funds whose long-term strategies are centred around investing in rental properties and that are looking to acquire housing complexes are now being outbid by (mostly Dutch) investors with a strategy of selling off rental properties to owner-occupiers. These parties then remain involved in the portfolio for a long period of time - often more than 20 years - in order to sell it completely on the private owner-occupied housing market.

The increased interest rates, higher transfer tax and regulatory impact will have a significant effect on property value if an investor wants to continue letting a home. In many cases, the above combination of factors is expected to cause a drop in value of as much as 20% to 30% compared to current book values. Investors with the strategy of selling off rental properties, on the other hand, set the offer price based on 65% to 75% of the vacant possession value (the price an individual property fetches in the owner-occupied market). With prices in the owner-occupied housing market on the rise again, this is giving these investors a higher bidding capacity.

Until 2021, bids from investors with a buy-to-let strategy tended to be higher than those from investors with a strategy of selling off rental properties. This situation has now been completely reversed. Indeed, in the past year a historically high proportion (48%) of existing housing portfolios were sold to investors with a strategy of selling off rental properties, which means that these properties will eventually disappear from the rental housing market.

Remarkably, further analysis shows that the majority (84%) of these individual properties will not be affected by the new mid-rent regulations. This implies that, in addition to the selling off of rental properties that will soon be subject to regulations, there will also be an additional wave of selling off rental properties in the unregulated segment, caused by the current economic situation and the deteriorating investment climate. At the moment, it appears that this wave will sweep up some 3,000 homes purchased since 2022. If the current price ratios between continuing to let and sell houses on the owner-occupied market remain stable, this number could rise to as many as 20,000 to 30,000 homes in the coming years.

As shown in Figure 8, the bulk of these residential units measure approximately 100 m². These are mostly multi-family homes in large cities, which often have a significantly higher turnover rate than single-family homes in medium-sized cities. Despite this higher turnover, these properties still form part of a long-term strategy. Investors with a sell-off strategy can often spend up to twenty years trying to sell all the homes individually. In future, this period could be longer still, assuming that turnover rates continue to decline to the level that we are already seeing to a large extent in the social rental sector.

Growing demand, falling stock

After years of strong growth, the rental housing market is now showing a significant contraction, partly as a result of policy and legislative changes that are having a strong adverse effect on the investment climate. If the proposed policy is not changed, this negative trend will continue in the years ahead. The introduction of rent control is set to push around 100,000 rental properties into the owner-occupied market. Ironically, these are almost exclusively homes that would otherwise be offered in the newly regulated mid-rent segment. Added to this is the loss of 20,000 to 30,000 rental homes due to the deteriorating investment climate and the current economic situation. As explained above, the vast majority (84%) of these are homes in the unregulated segment, and this impact would be in addition to the possible adverse effects of tax changes.

Moreover, there is no reason to assume that the rental stock will recover any time in the near future. In recent years, investors added an average of 14,000 homes to the stock every year. Given the current deterioration in the investment climate, this volume is likely to fall back to the pre-2015 level of 6,300 homes per year. In short, despite the potential addition of new-build homes, the rental stock will still decline significantly, which will automatically lead to further rent increases in the unregulated segment.

Moreover, if the investor-owned rental stock declines by 17%, this will make the rental housing market – which can be seen as the flexible shell of the overall housing market – much less accessible. Ultimately, this reduced accessibility will also affect the dynamics in the social housing segment and the owner-occupied market, as moving will become more difficult for everyone. A knock-on effect on the labour market can also be expected, as talented jobseekers will find it difficult to move to other regions. This will have a limiting effect on future economic productivity in the Netherlands. It is therefore necessary to minimize the negative impact of regulatory measures on the availability of rental housing, so that mobility in the housing and labour market is guaranteed and economic productivity is not compromised.

Most recent reports

-

The logistics market is entering a new phase. Following a period of growth, which peaked during the Covid-19 pandemic, it is now giving way to consolidation.

-

Report | Intelligent Investment

European Life Sciences Ecosystems: Sector Guide 2026

The European life sciences sector is a key contributor to global innovation and growth, propelled by technological breakthroughs, expanding scientific platforms, and a robust pipeline of novel therapies.

-

How the 25 most expensive retail streets adapt to shifting consumer behavior and economic pressures.

-

Report | Intelligent Investment

European Hotels Destination Index

CBRE’s European Hotels Destination Index ranks 66 cities by market pillars and economic fundamentals to highlight top hotel investment opportunities.