Viewpoint

Larger shopping centres are regaining investor interest

August 21, 2025 9 Minute Read

After years of digitalisation and restructuring, the Dutch retail market is entering calmer waters. There is renewed potential for growth, particularly in larger, planned shopping centres. These centres offer economies of scale, strategic locations, and multifunctionality, making them an attractive proposition for investors focused on value creation.

Retail market regains balance following years of rapid e-commerce expansion

Over the past two decades, the Dutch retail market has undergone a profound transformation. While the early 2000s saw rapid expansion in retail floor space, that trend has now reversed. Despite a population increase of nearly two million since 2005, the retail stock has barely grown, resulting in a decline in retail space per capita. At the same time, the rise of e-commerce triggered a necessary restructuring of the retail landscape; a phase that is now largely complete. Retailers have refined their omnichannel strategies and are leveraging physical stores as integral components of the customer journey.

Developments in the retail landscape, 2005–2030

|

Year |

Population (mln) |

Retail space per capita (sqm) |

E-commerce share (%) |

Vacancy (sqm) |

Retail sales per sqm* |

Retail investment share (%) |

|

2005 |

16.305 |

2.31 |

2.0% |

5.5% |

€ 4,131 |

36% |

|

2013 |

16.779 |

2.41 |

7.5% |

7.6% |

€ 3,243 |

15% |

|

2019 |

17.282 |

2.39 |

15.1% |

7.8% |

€ 3,677 |

9% |

|

2025 |

18.082 |

2.31 |

23.4% |

5.4% |

€ 3,834 |

18% (H1) |

|

2030 |

18.475 |

2.26 |

27.8% |

|

€ 4,134 |

|

Source: CBRE Research

The result is a balanced market: retail turnover per square metre is increasing, vacancy has returned to a healthy frictional level, and investor confidence is recovering. In the first quarter of 2025, the share of retail in total investment volume rose to 18%. Although this was partly driven by a few large transactions, it clearly signals renewed interest in retail real estate, particularly in larger shopping centres. The recent sale of several major centres, which had not changed ownership for years, shows that investors once again see potential in these locations and have confidence in profitable operations and long-term value creation.

Read more about recent transactions involving larger planned shopping centres and their investment potential in our full report.

Investors shift focus to planned shopping centres

In the first half of 2025, nearly €900 million was invested in retail properties. This means that after just six months, investment volume is already close to the full-year total for 2024, a strong indication of renewed confidence and momentum in the retail investment market. Investor sentiment appears to be shifting: institutional investors and private equity are showing renewed interest, marking the onset of a new investment cycle.

Notably, a large share of transactions involved larger, planned shopping centres: over € 415 million, including Stadshart Zoetermeer (€ 150 million), Leidsche Rijn Centrum (€ 95 million), Winkelhof Leiderdorp (€ 55.5 million), and Sint-Jorisplein Amersfoort (€ 27.5 million). This marks a clear break from the trend in 2023 and 2024, when few major retail transactions occurred and larger centres rarely changed ownership.

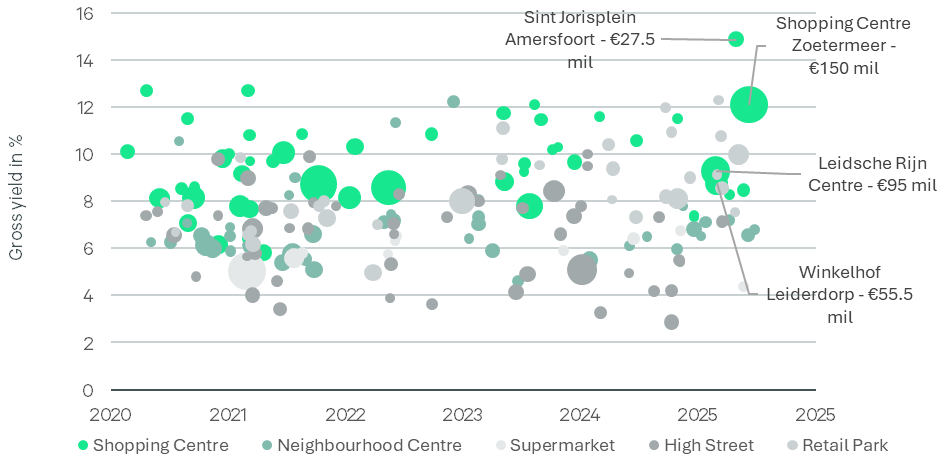

Retail investment market developments, 2020–2025H1

Several years ago, the market began to shift towards smaller, planned retail centres. This movement gained additional momentum during the COVID-19 pandemic.

During that period, neighbourhood centres with a high share of supermarkets (over 50%) and convenience retail (over 70%) proved their value as stable and crisis-resilient investments. Investors are now also willing to invest in medium-sized and large planned centres again. The risk profile of these centres no longer differs significantly from that of smaller centres, partly due to attractive initial yields and relatively low prices per square metre.

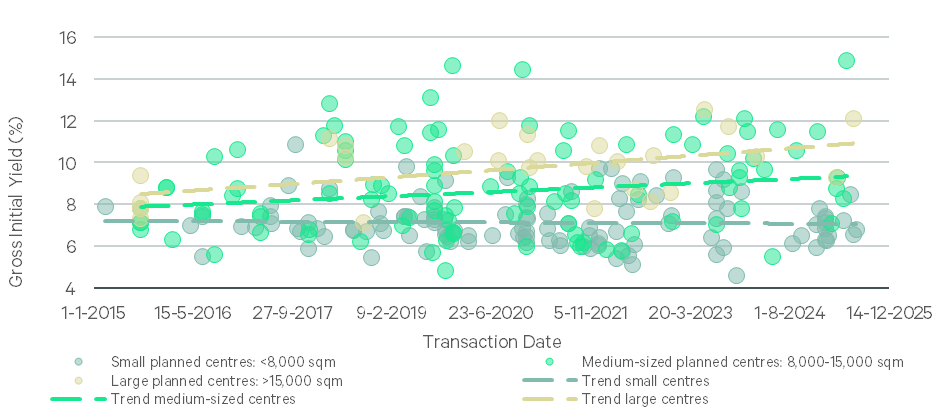

Development of gross initial yields for different types of planned centres, 2015–2025H1

In 2015, gross initial yields for planned shopping centres typically ranged between 7% and 9%. By 2025, the differences are significantly greater: smaller centres show slight yield compression, while medium-sized and large centres offer higher yields of 8–10% and 10–12%, respectively. Now that the investment cycle has turned, an attractive entry point is emerging for investors looking to benefit from the current yield potential.

Larger planned centres offer opportunities and require attention

Medium-sized and large centres tend to have more fashion retail and less convenience-oriented retail. The share of hospitality and cultural functions does not differ significantly between larger and smaller planned centres. Larger planned centres show slightly higher vacancy and turnover rates, indicating a higher risk profile, but this dynamic also creates opportunities for repositioning. Tenant turnover provides room to optimise the retail mix and better align it with local market demand and the lifestyles present in the catchment area. Our full report explores which types of planned shopping centres offer opportunities for repositioning and the development of dominant retail concepts.

Characteristics of planned shopping centres by size category

|

Large planned centres >15,000 sqm |

Medium-sized planned centres 8,000– 15,000 sqm |

Small planned centres <8,000 sqm |

|

|

Vacancy rate (Q2-2025) |

10.4% |

9.8% |

8.8% |

|

Turnover rate (2024) |

10.5% |

9.1% |

8.0% |

|

Share of convenience retail |

22% |

33% |

53% |

|

Average number of supermarkets |

2.1 |

1.7 |

1.2 |

|

Share of fashion |

36% |

28% |

15% |

|

Share of hospitality & culture |

13% |

13% |

10% |

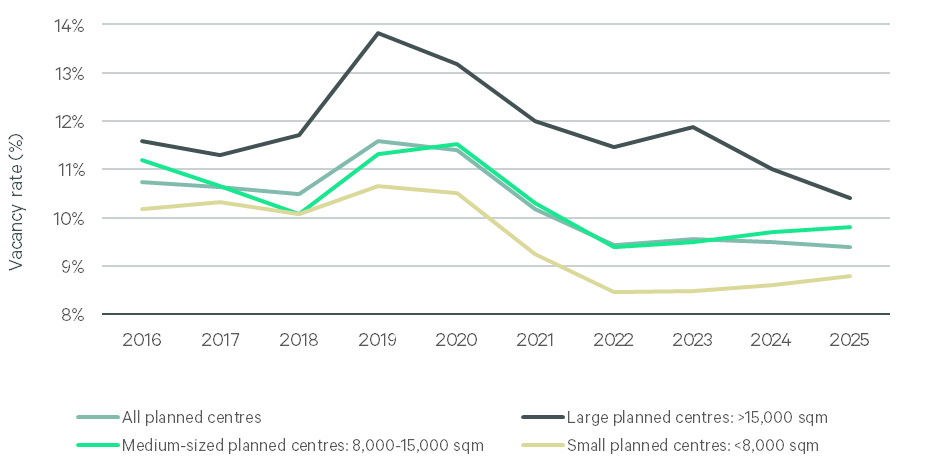

Despite the disappearance of brands such as Blokker and D-Reizen, vacancy in large centres continues to decline steadily. The gap with smaller centres has narrowed significantly. At 10.4 percent, vacancy in large planned centres is now at its lowest level in the past decade, and considerably lower than the 13.8 percent recorded in 2019. The combination of falling vacancy and rising yields suggests that risks may have been overestimated. This presents opportunities for investors who are willing to step in while others remain cautious.

The combination of declining vacancy, stable performance and attractive yields is making larger planned shopping centres appealing to investors once again. Institutional investors are also expected to refocus their attention on this type of real estate. As a result, these assets are likely to see a decline in initial yields.

Vacancy trends 2015–2025Q2 by type of planned shopping centre

Four types of retail centres: opportunities and strategies per quadrant

Medium-sized and large planned retail centres differ significantly from one another. A high share of convenience retail helps reduce the risk of vacancy. Fashion is present in nearly all centres, but as its share increases, so does the risk profile. From an investment perspective, fashion tends to cause more vacancy than convenience retail, which calls for a critical view on tenant composition.

In total, there are around ninety larger centres with vacancy levels at or below the frictional threshold. These locations benefit from stable occupancy, strong footfall, and reliable rental income. In contrast, nearly one hundred centres, together accounting for over 1.5 million square meters, face vacancy rates of seven percent or higher. This indicates clear potential for improvement.

Whether a centre is medium-sized or large, all types of planned retail centres offer opportunities to improve spatial layout, retail mix, and functional integration. There is also room to optimise store formats and better align them with the needs of the catchment area.

Focused asset management can transform these centres into future-proof locations with a clear structure and logical clustering of functions. This creates environments that respond to changing consumer behaviour, in which fast and functional shopping and leisure-oriented shopping are central. At the same time, these centres vary widely in scale, focus, and characteristics. Four distinct types can be identified based on vacancy levels and the share of convenience retail. Each type presents its own opportunities, risks, and corresponding investment strategies.

Find out in our full report, featuring examples of recent transactions from Stadshart Zoetermeer and Leidsche Rijn Centre.

Read the full viewpoint here

Retail insights

-

Dutch retail parks are showing resilience: stable rental income, low vacancy rates, and attractive returns for investors.

-

In this publication, we share our expectations for the most important developments in the real estate investment market in 2026.

-

Discover the evolving real estate market cycle for the year. Learn why elevated interest rates, income-driven returns, and proactive asset management are key. Explore growth in the living sector and data centers amidst improving financing conditions.

-

How the 25 most expensive retail streets adapt to shifting consumer behavior and economic pressures.

-

Viewpoint | Intelligent Investment

Larger shopping centres are regaining investor interest

August 21, 2025

Dutch retail is regaining its footing after a decade of transformation. Larger shopping centres are attracting renewed investor interest, fueled by attractive yields and repositioning potential.

-

Book | Intelligent Investment

European Real Estate Market Outlook Mid-Year Review 2025

August 7, 2025

Welcome to CBRE’s 2025 European Mid-Year Market Outlook. In this report, we revisit the predictions we made at the beginning of the year, assess their accuracy, and share our perspective for the months ahead.

-

Report | Intelligent Investment

Mid Year Real Estate Market Outlook 2025 The Netherlands

July 17, 2025

The Dutch real estate investment market is recovering in the first half of 2025. Despite geopolitical uncertainty, the market is in an upward cycle, though recovery speeds vary across sectors, partly due to less international investment.

-

In CBRE's Real Estate Market Outlook 2025, you will discover the latest real estate trends. From economic stability to investment opportunities: you can read it in our publication.