Market Intelligence

PJM’s Reliability Backstop Procurement: Implications for capacity costs and reliability

April 15, 2026 5 Minute Read

What Happened

On April 10, PJM released its proposal for a Reliability Backstop Procurement (RBP), a one-time capacity procurement to secure nearly 15 GW of new power supply that can come online by June 2031.

The RBP is designed to address the region's growing electricity shortfall as part of the ongoing Critical Issue Fast Path (CIFP) program. PJM expects to file for approval of the RBP with the Federal Energy Regulatory Commission (FERC) in June 2026.

Market Analysis

PJM's RBP is unlikely to lower power or capacity prices for ratepayers. The program would allow data centers to secure most, if not all, of the new gas and battery supply that can come online by mid-2031, removing those power plants from the region's yearly capacity auctions.

These bilateral contracts would reduce some data center load in PJM's reliability targets. However, the remaining demand would still compete for limited new supply in future capacity auctions, likely putting more pressure on clearing prices.

How PJM's RBP Would Work

In Phase I of the RBP, data centers and load-serving entities can negotiate bilateral capacity contracts directly with new supply projects between September 2026 and March 2027. Price and contract length would be set privately by the negotiating parties.

After March 2027, PJM would hold a central procurement to acquire any remaining capacity needed to reach the 15 GW target. Each electric distribution company (EDC) still facing a shortfall after Phase I would need to participate. PJM would set a price cap and contract duration of 2 to 15 years. The resulting Phase II capacity costs would flow through to all customers in each participating EDC.

The few gas and battery projects that can come online by June 2031 will likely contract only with data centers in Phase I. Few projects that can energize by mid-2031, if any, would remain available to Phase II buyers. This will likely narrow the options for PJM's EDCs to readily-available demand response or distributed energy resources.

Table 1. Overview of Key Reliability Backstop Procurement Provisions in the April 10, 2026 Proposal

Cost and Reliability Outlook

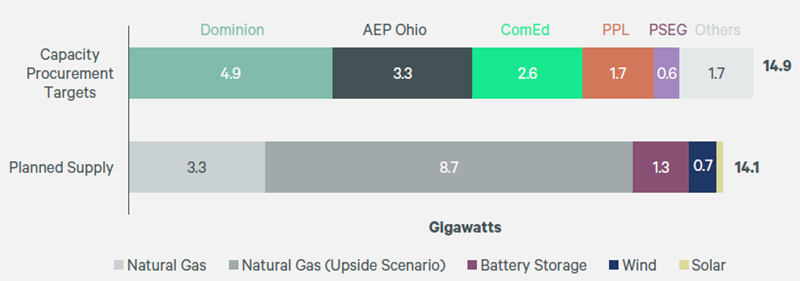

The pool of large gas and battery projects that could come online before the mid-2031 deadline will likely fall below PJM's RBP target of 15 GW, even if an additional 8.7 GW of gas plants that reportedly secured equipment energize on time. Less than 5 GW of gas and battery storage in PJM's interconnection queue have reported plans to commission before the deadline. Some of these projects could be also facing delays due to well-documented equipment shortages. Demand response and distributed energy resources would be eligible to bid into both phases. Unlike big power plants, these resources do not face PJM grid queue delays and could be operational well before the June 2031 deadline.

Limited supply likely gives the few developers with shovel-ready projects pricing power during Phase I of the RBP program. Data centers, which face aggressive build-out timelines, may be willing to pay premium prices for capacity that can be delivered before the mid-2031 deadline. Project developers will also need to absorb all transmission upgrade costs identified through PJM's interconnection process. Because developers bear network upgrade costs, including any overruns beyond their initial estimates, they may be incentivized to pad their bids during both phases of the program.

While PJM's annual capacity auctions reset prices each year, new backstop commitments could run for up to 15 years. High prices negotiated through the RBP in Phase II could remain on customer bills through the mid-2040s. Other ratepayers in EDCs not facing a supply shortfall could benefit from new supply secured in Phase II entering PJM's BRA at $0/MW-day, which would increase available capacity and put downward pressure on clearing prices.

Figure 1. Projected Capacity Shortfall by PJM EDC vs New Reliability-Adjusted Supply Under Development in PJM and Expected to Come Online On or Before June 1, 2031.

Energy Solutions

Accelerate your decarbonization efforts by transitioning to clean energy sources.