Adaptive Spaces

2026 U.S. Industrial & Logistics Occupier Survey

No Slowdown in Demand for Industrial Space

April 6, 2026 5 Minute Read

Executive Summary

- A majority of industrial occupiers expect to either maintain or expand their real estate footprint this year, according to a recent CBRE survey. Those with expansion plans are mainly targeting the Southeast and are expressing a growing reliance on third-party logistics providers (3PLs).

- Occupiers are showing a clear preference for newer, high-quality facilities despite rising rents and occupancy costs. Nearly half of survey respondents with manufacturing operations in the U.S. plan to increase domestic manufacturing to shorten production time and gain faster access to U.S. consumers.

- Most occupiers anticipate only a moderate operational impact from trade policy changes and report limited plans to integrate artificial intelligence into their logistics strategies.

- Taken together, these insights suggest that while caution remains amid high costs, occupiers continue to position their real estate portfolios for long-term efficiency and growth.

- The survey was conducted in early Q1 2026 before the outbreak of the Middle East conflict.

Demand Outlook

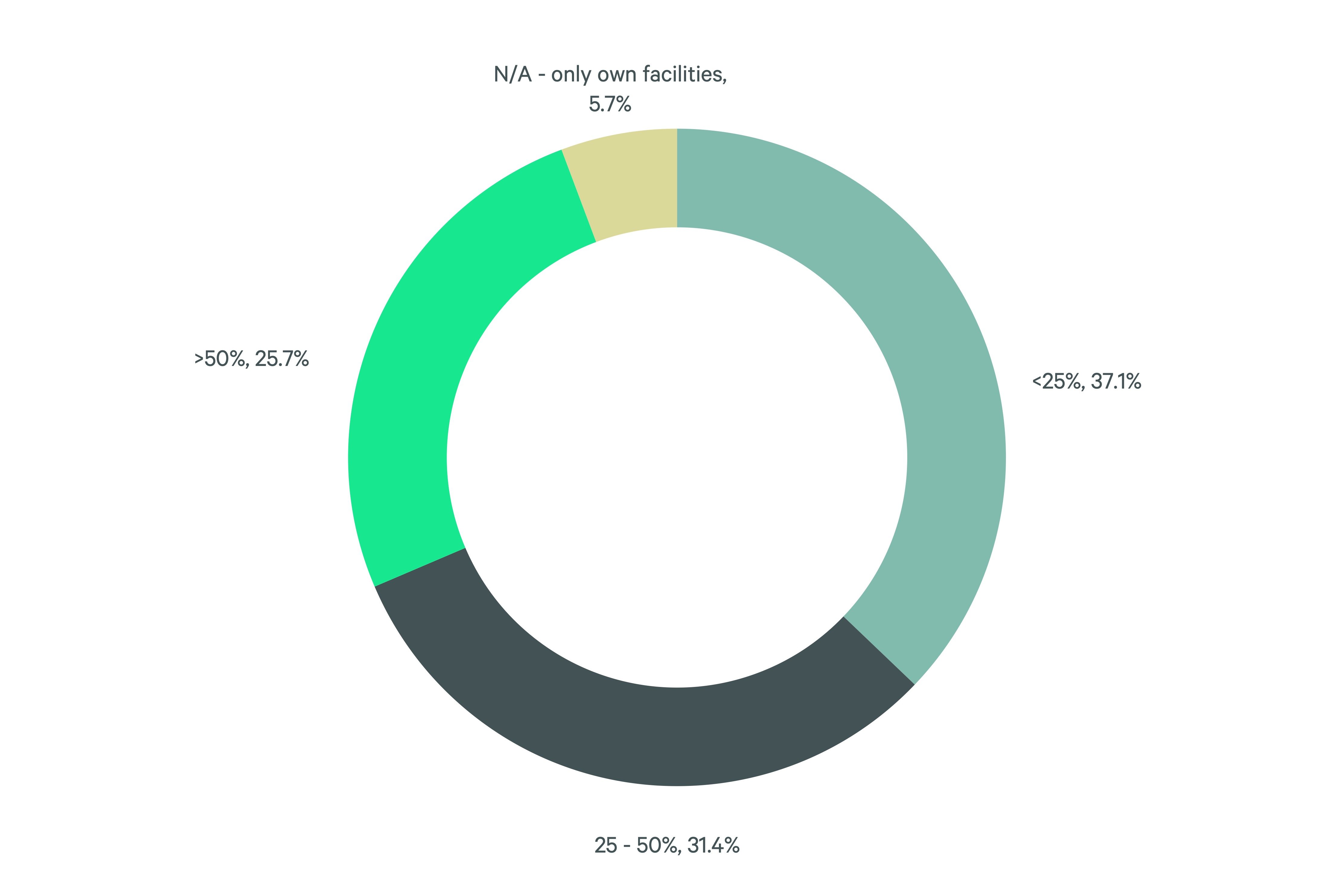

- Nearly 67% of respondents indicated that more than 25% of their leases will expire over the next 36 months. CBRE Research estimates these lease expirations will total more than 1.7 billion sq. ft. This means that the market is entering a major renegotiation cycle that may require more concessions by landlords to secure or retain tenants.

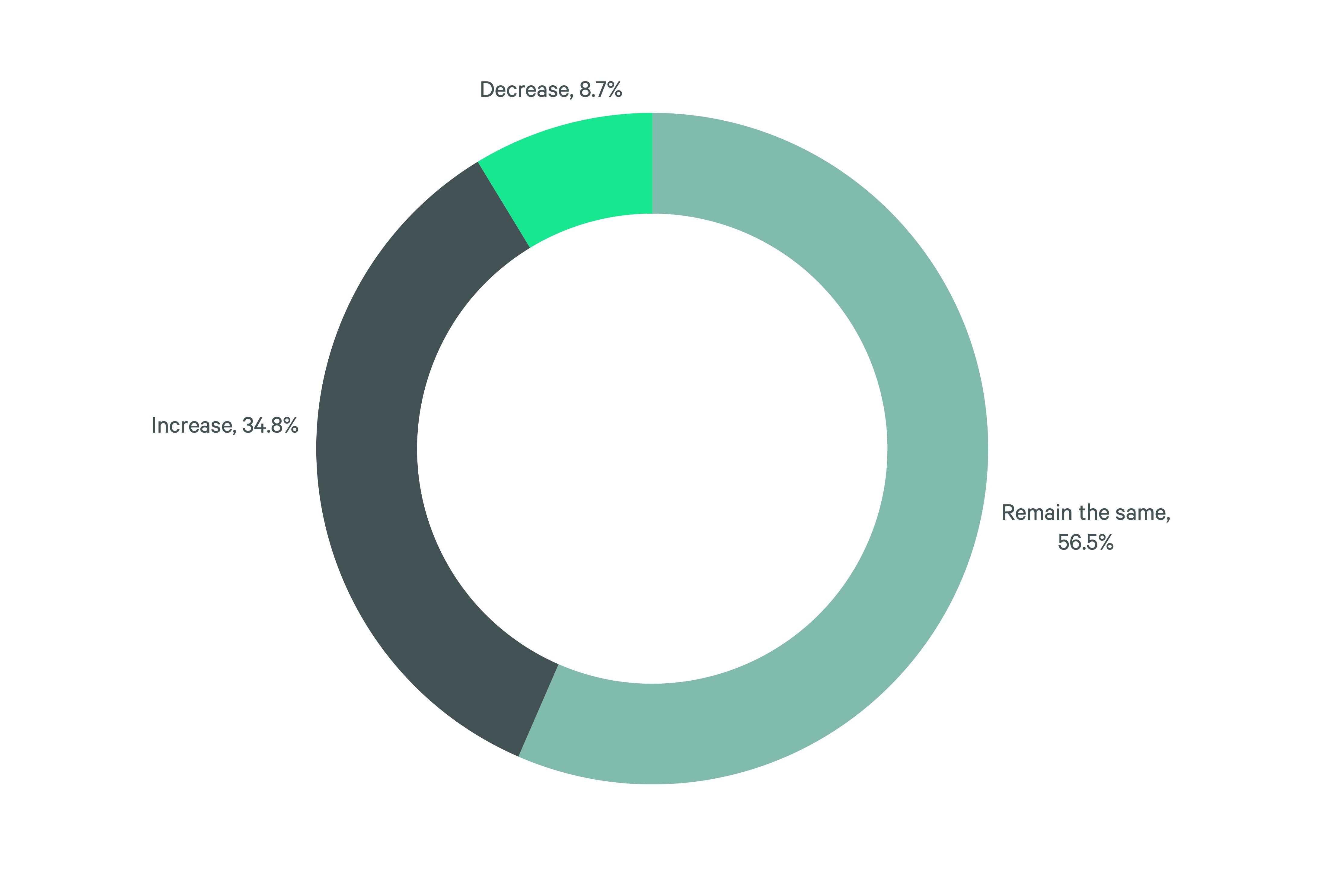

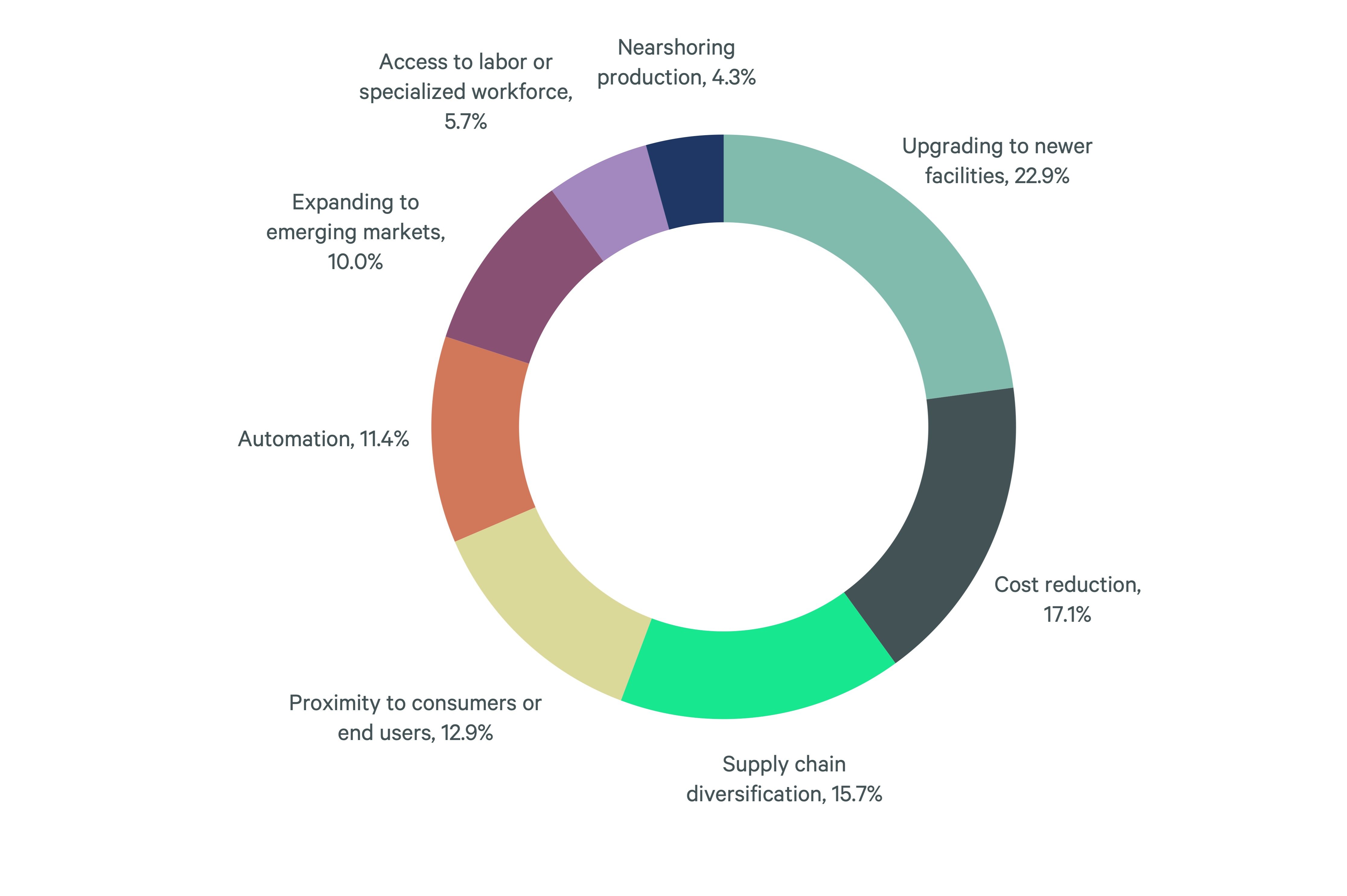

- Over 90% of respondents plan to maintain or expand their real estate portfolio over the next 36 months, with 23% interested in upgrading to newer facilities and 17% looking to reduce costs. This indicates a continued consolidation of pre-2020 facilities, which posted more than 400 million sq. ft. of negative net absorption in the past three years alone.

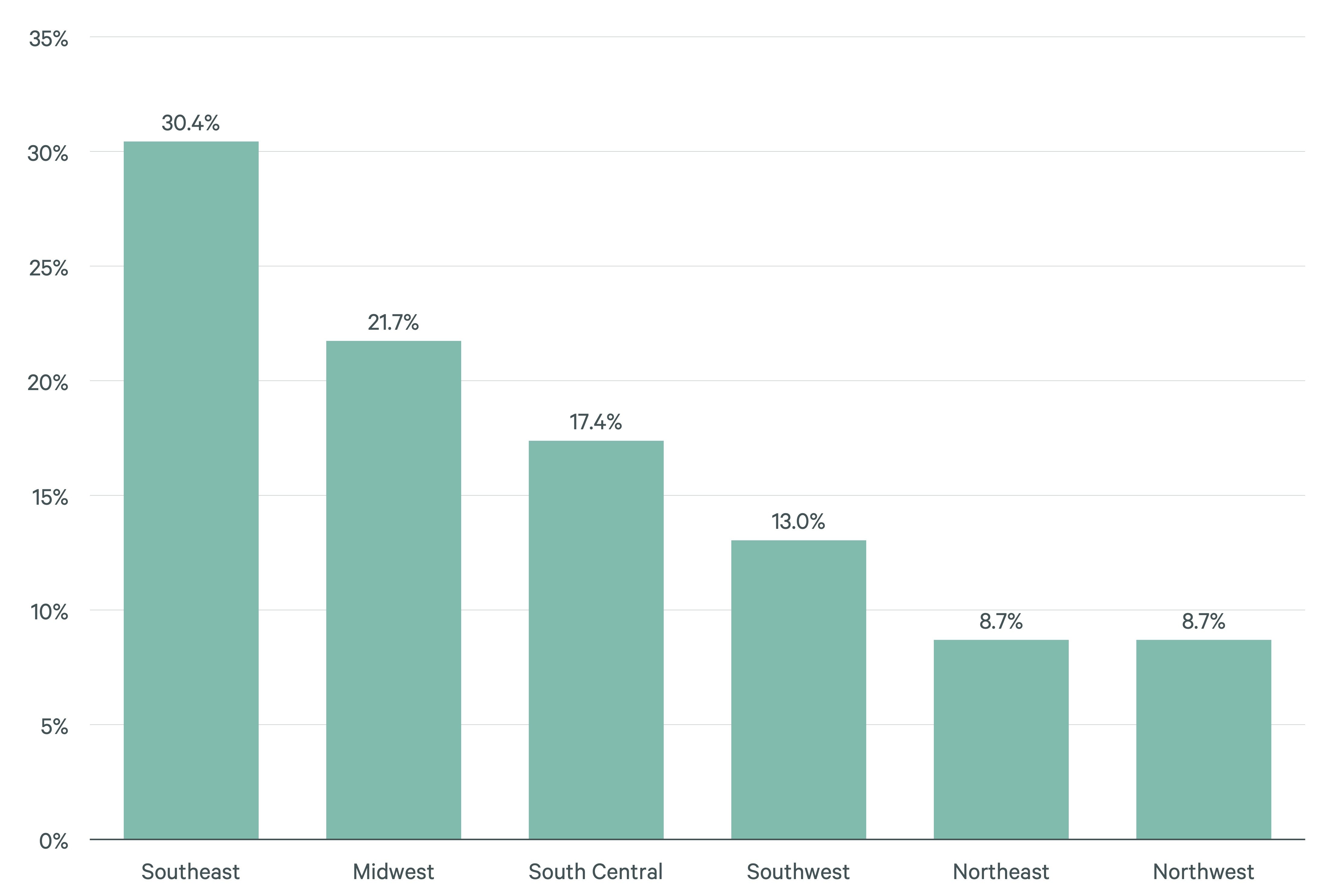

- The Southeast is the top region of choice for expansion over the next 36 months (30%), followed by the Midwest (22%). The Southeast offers a plethora of available newly constructed facilities, close proximity to growing population centers and a burgeoning manufacturing sector—all drivers of occupier site selection.

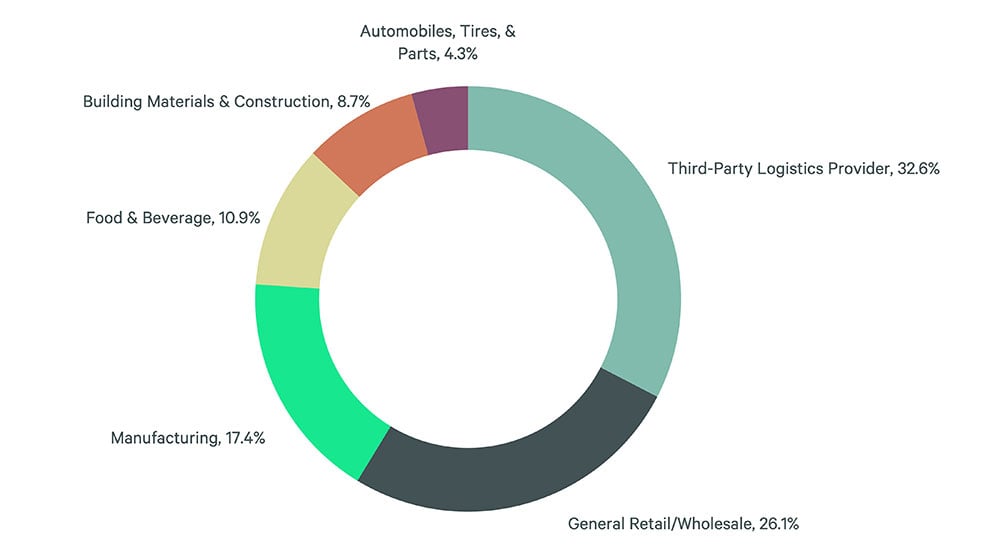

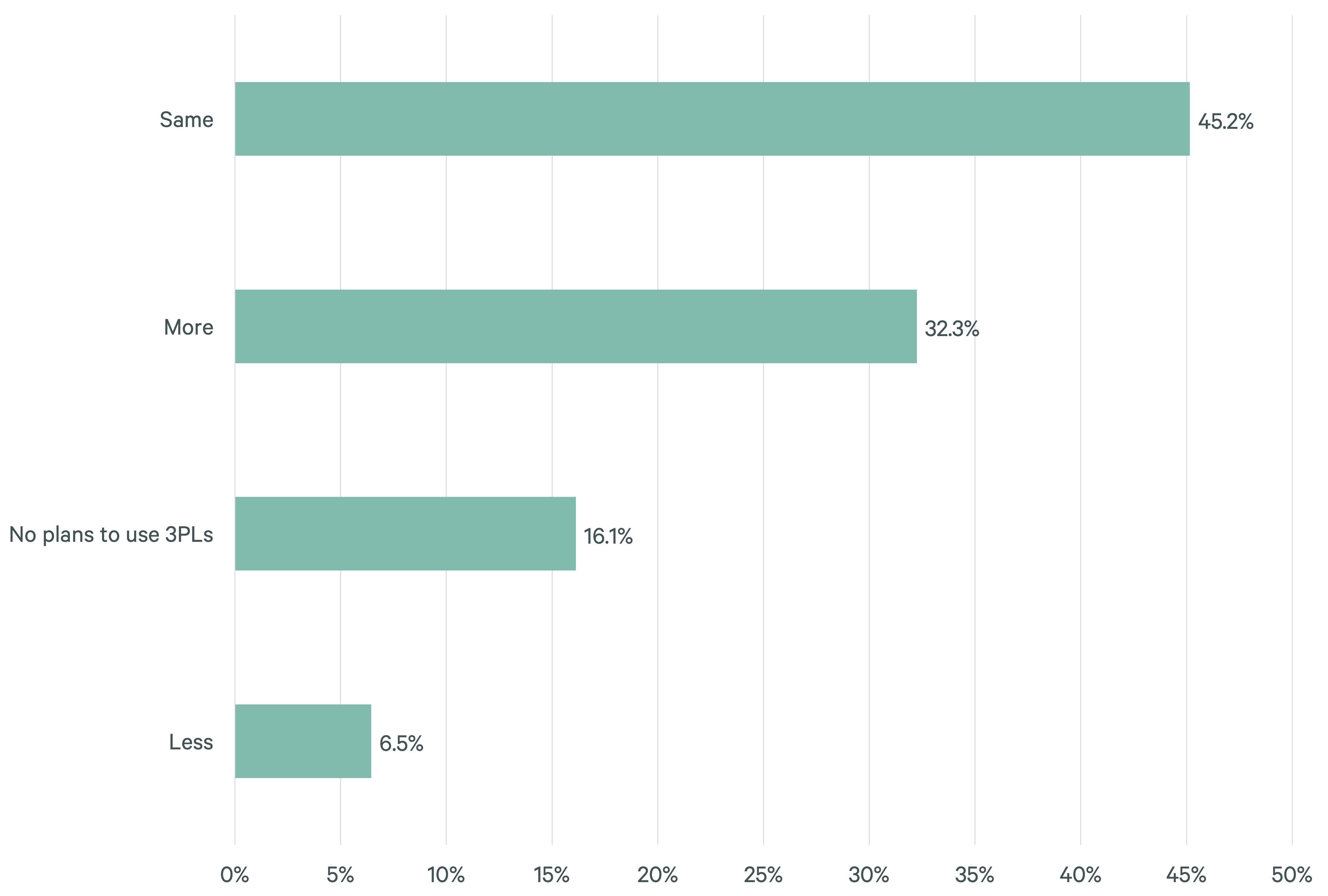

- 3PLs were the most active tenant base for bulk leases (100,000+ sq, ft,) in 2025 with a market share of 36% and are expected to remain so this year. Over 32% of survey respondents plan to increase their use of 3PLs over the next three years.

Figure 1: What best describes your company's primary business activity?

Figure 2: Approximately what percentage of your leases are expiring over the next 36 months?

Figure 3: How do you expect your warehouse/manufacturing requirements to change over the next 36 months?

Figure 4: What regions are you are looking into for expansion over the next 36 months? (select up to 3)

Figure 5: At what rate do you plan to use third-party logistics providers over the next 36 months?

Manufacturing

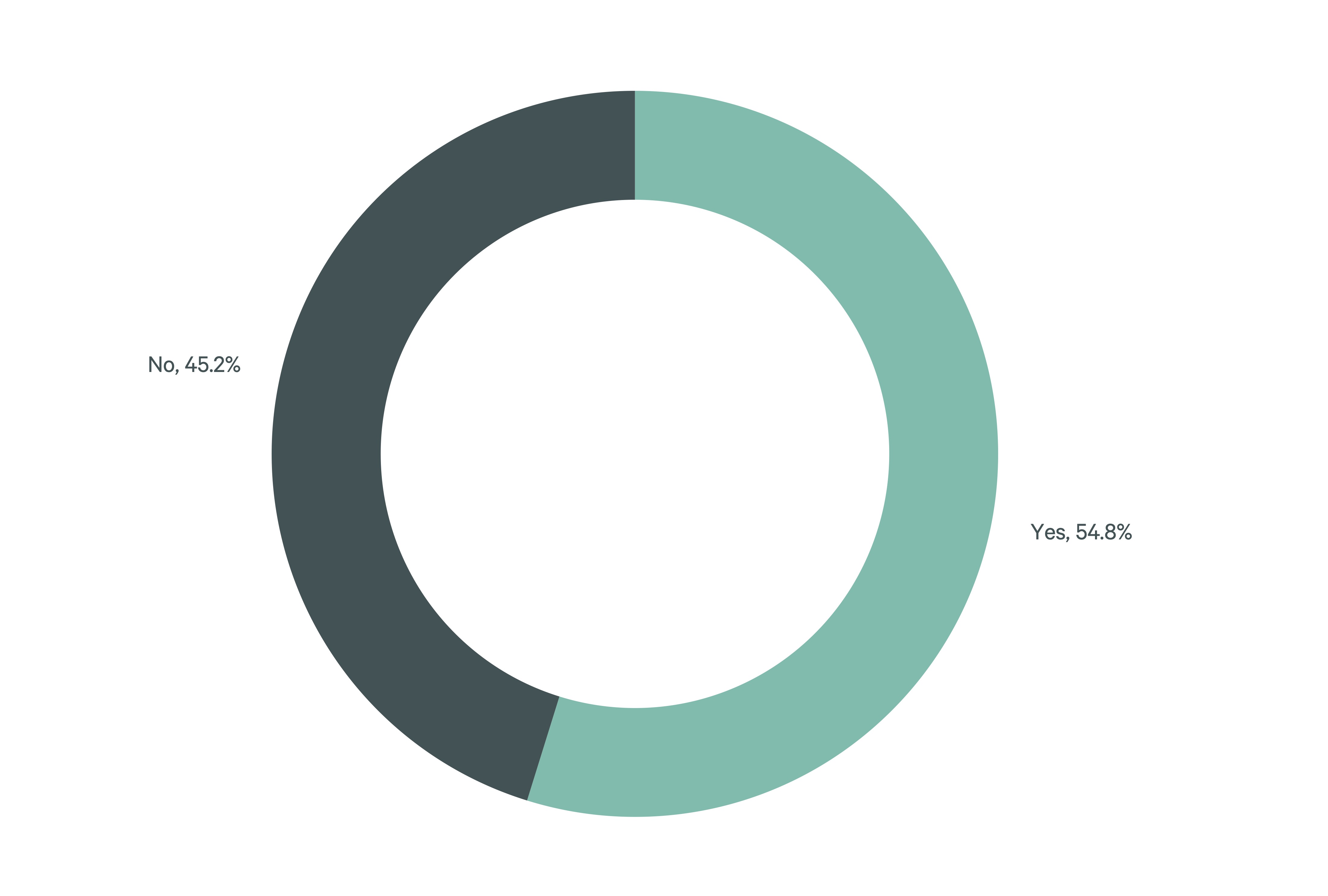

- Just over 50% of companies with manufacturing operations in the U.S. are actively expanding those operations or plan to do so in the next 36 months.

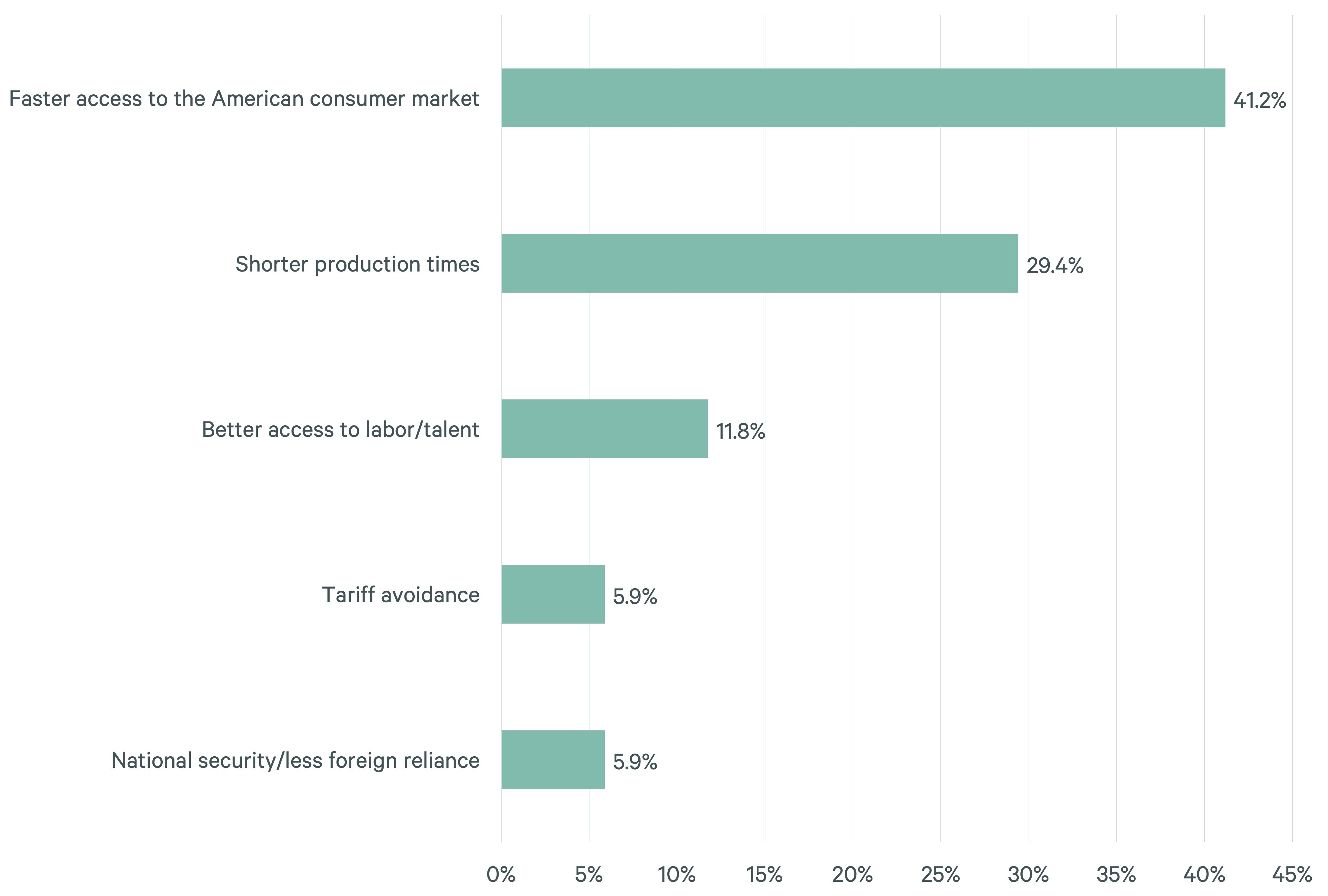

- Forty-one percent of survey respondents said that protecting domestic inventory to serve American consumers, rather than avoiding tariffs, is the major reason for expanding their U.S. manufacturing operations. Twenty-nine percent cited shorter production times as the major reason, while only 6% cited tariff avoidance.

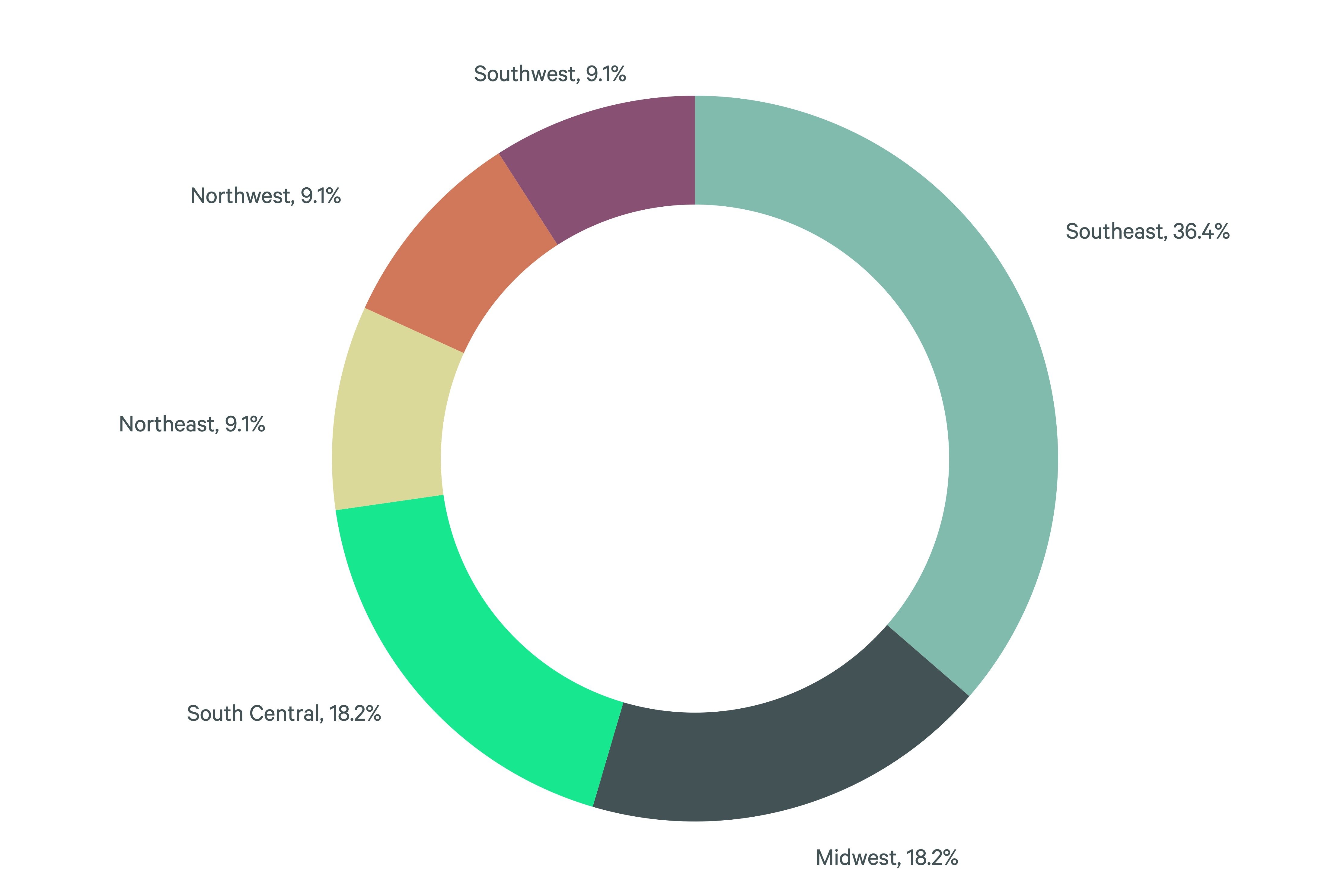

- The Southeast is the top region for 36% of respondents that plan to expand their manufacturing operations. The region’s population growth, pro-business environment and convenient seaports in Charleston, Savannah and Norfolk were cited as the main reasons of interest by occupiers.

Figure 6: Percentage of non-3PL survey respondents with U.S. manufacturing operations

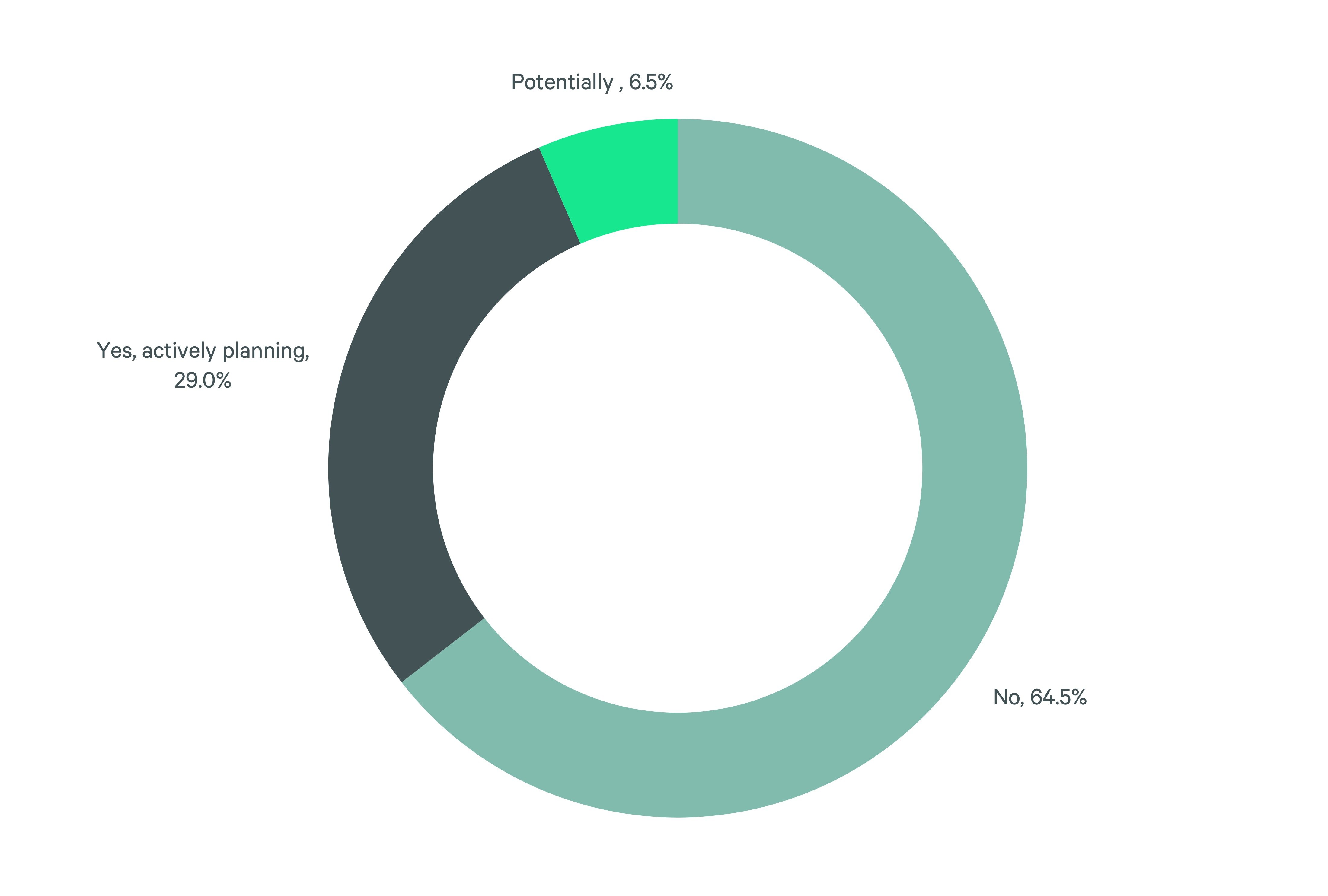

Figure 7: If not currently manufacturing in the U.S., are you planning to in the next 36 months?

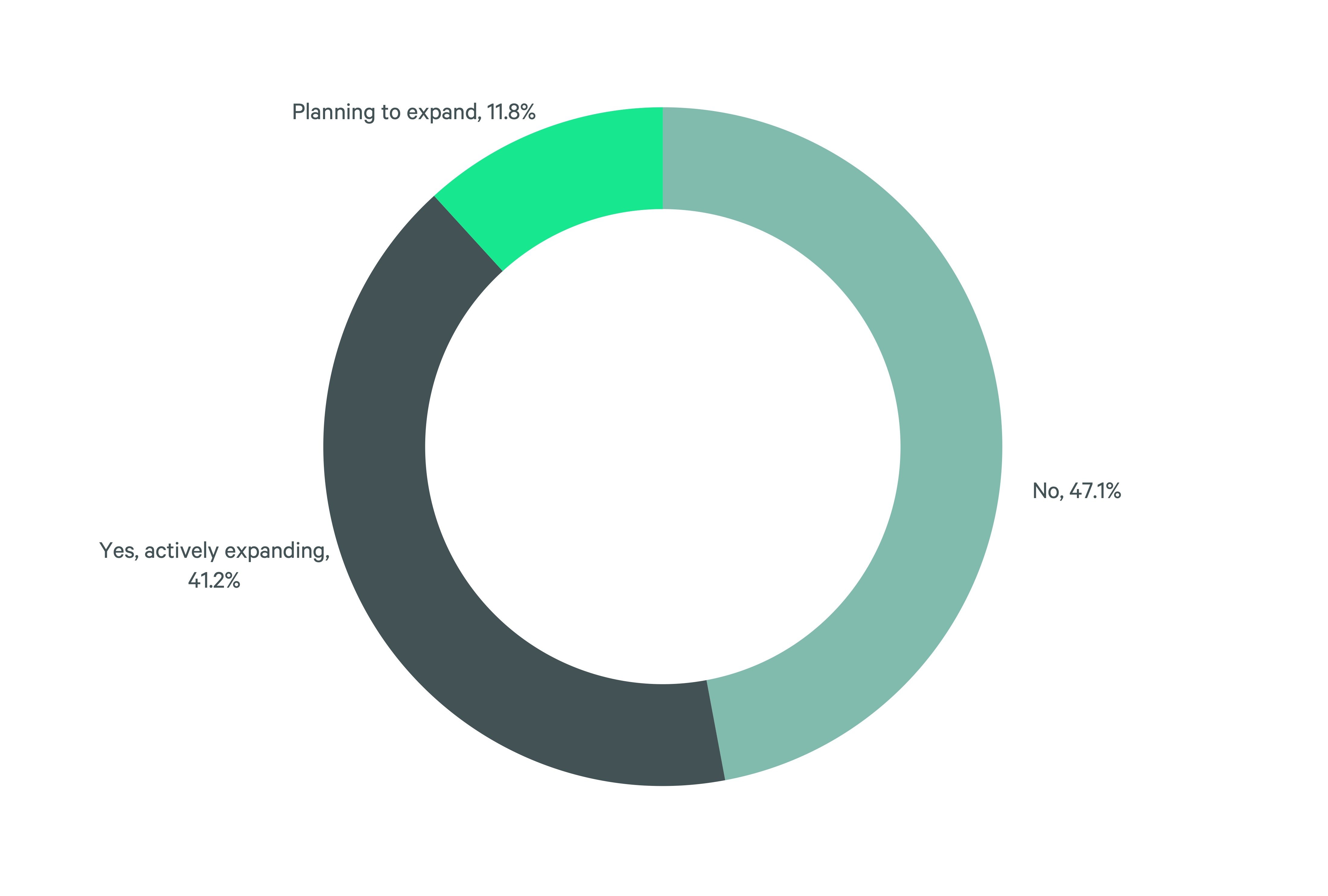

Figure 8: Do you plan to expand domestic manufacturing if you are currently manufacturing in the U.S.?

Figure 9: If you plan to expand manufacturing, what are the major reasons for doing so? (select up to 3)

Figure 10: If planning to expand manufacturing, what region are you focused on? (select up to 3)

Challenges & Opportunities

- Occupancy-related costs are by far the top challenge for occupiers this year, influencing their real estate decision-making, location strategy and business operations.

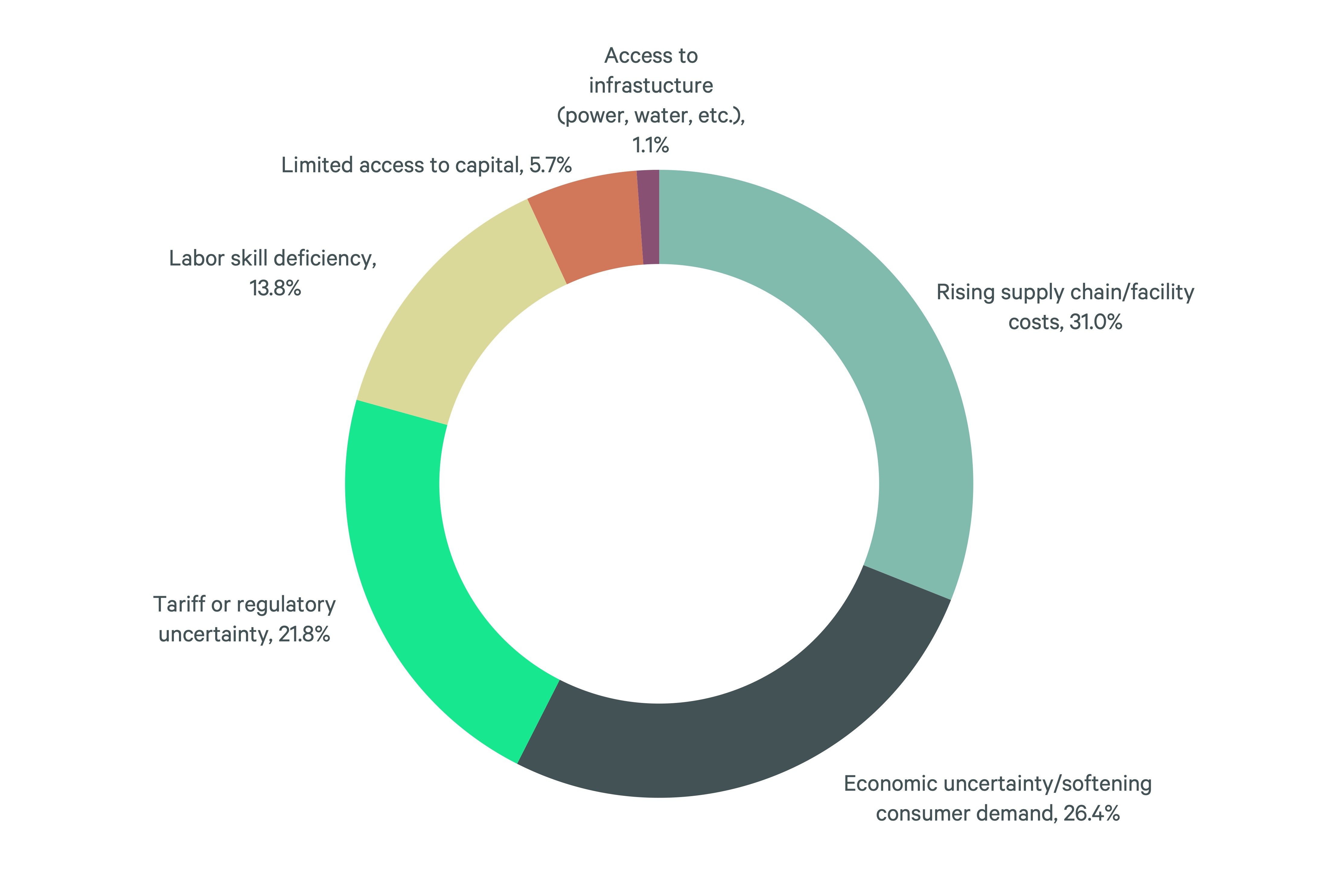

- Rising supply-chain-related costs (construction, energy, labor, insurance and transportation), economic uncertainty/softening consumer demand and tariff/regulatory uncertainty are the top three business challenges for industrial occupiers this year.

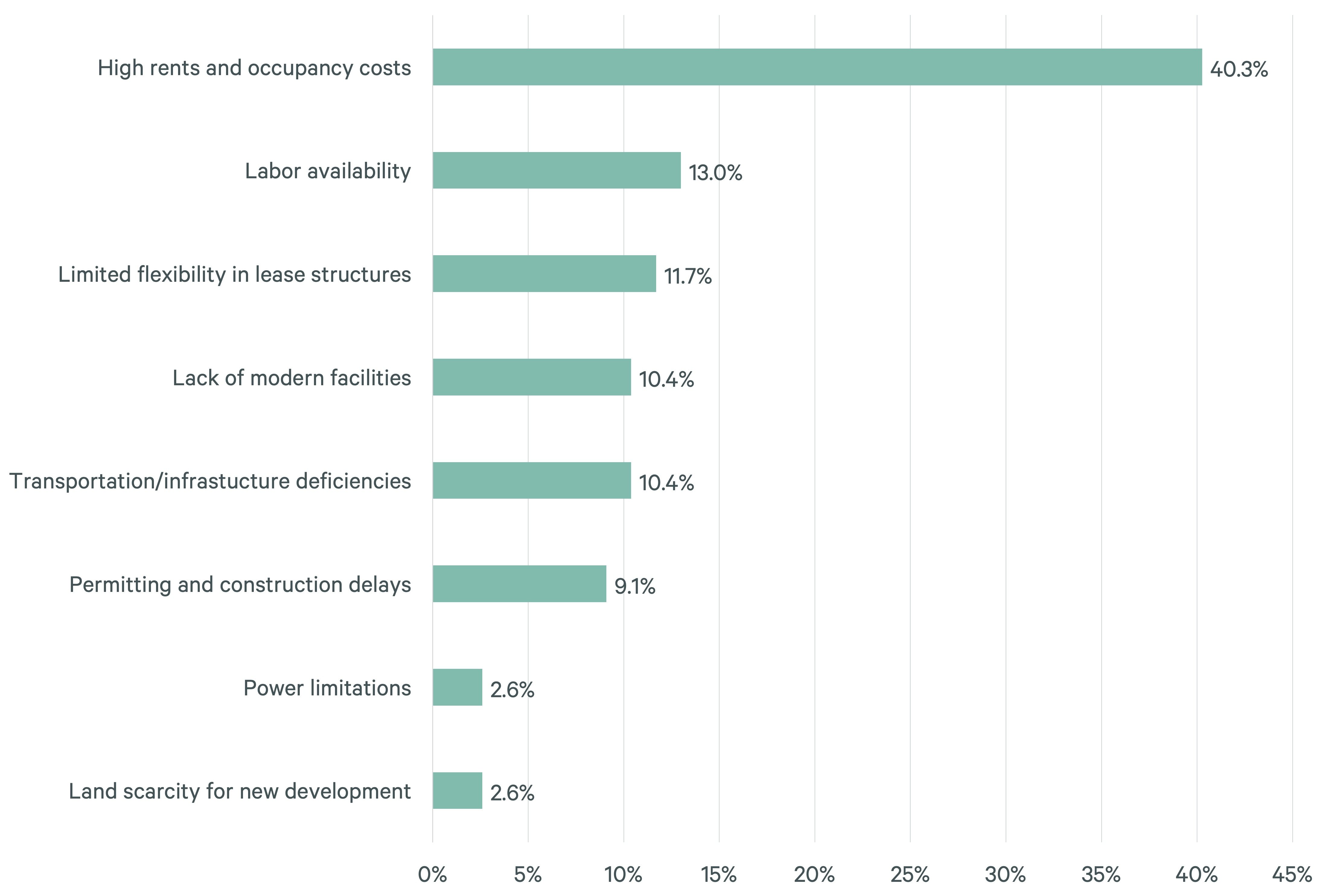

- High rents and occupancy costs are the top real-estate-related challenge for 40% of respondents, followed by labor availability for 13%. CBRE calculates that an occupier with a five-year lease expiring at the end of 2025 can expect an average 27% increase in rent upon renewal. Northern-Central New Jersey, Houston and South Florida can expect a doubling of rent. Hence, occupiers are actively looking to optimize their portfolios and increase efficiency.

- When selecting markets in which to locate, 23% of respondents cited space availability in recently constructed buildings as the top factor, followed by lower costs (17%) and supply chain diversification (16%).

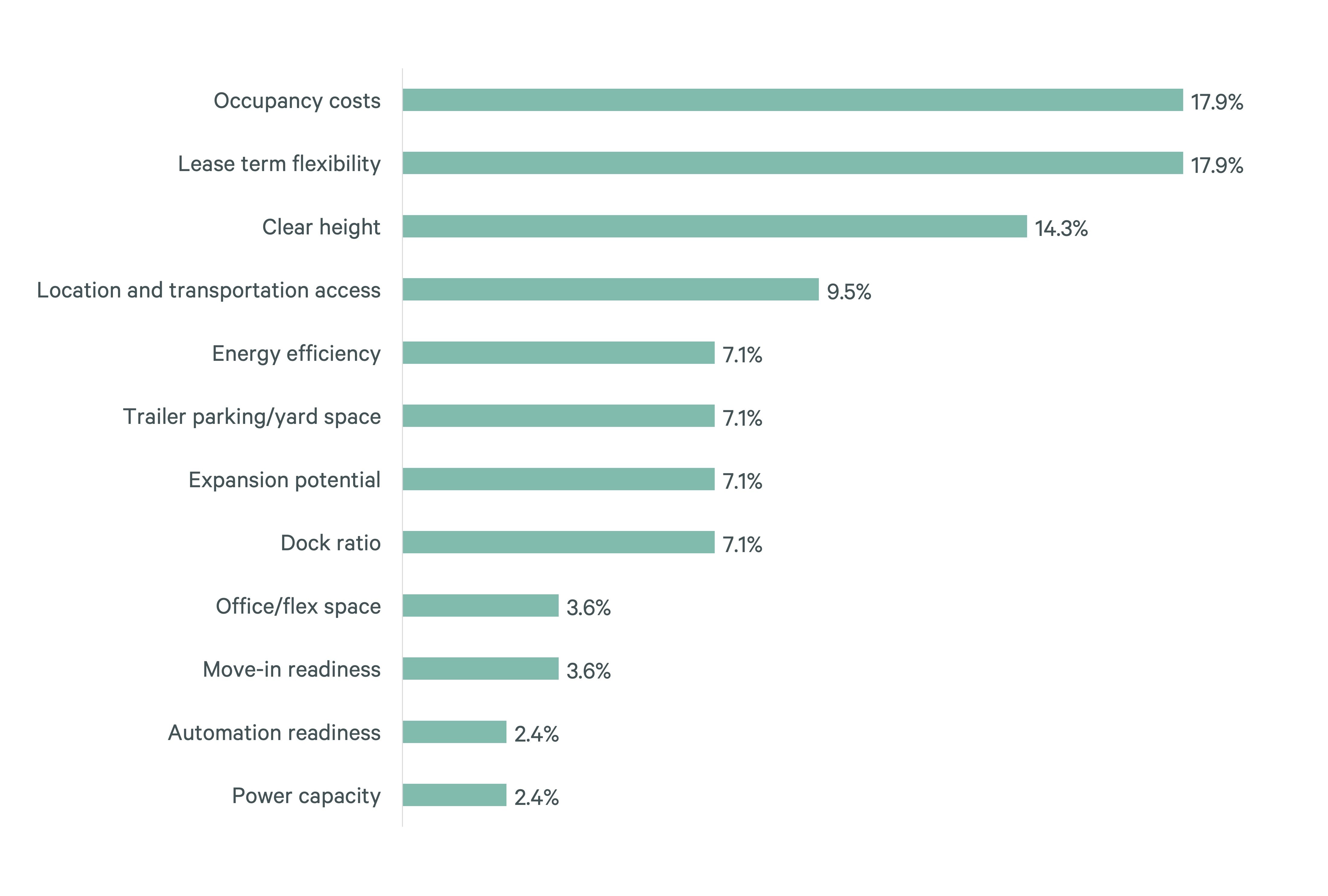

- Among the top factors for building selection, occupancy costs and flexible lease terms (ability to extend leases, options to purchase) were each selected by 18% of respondents. Clear ceiling heights (14%) and transportation access (10%) rounded out the top factors, while only 2% said power capacity. By combining market and building criteria, it is clear that cost, lease flexibility and close proximity to transportation hubs are top of mind for occupiers.

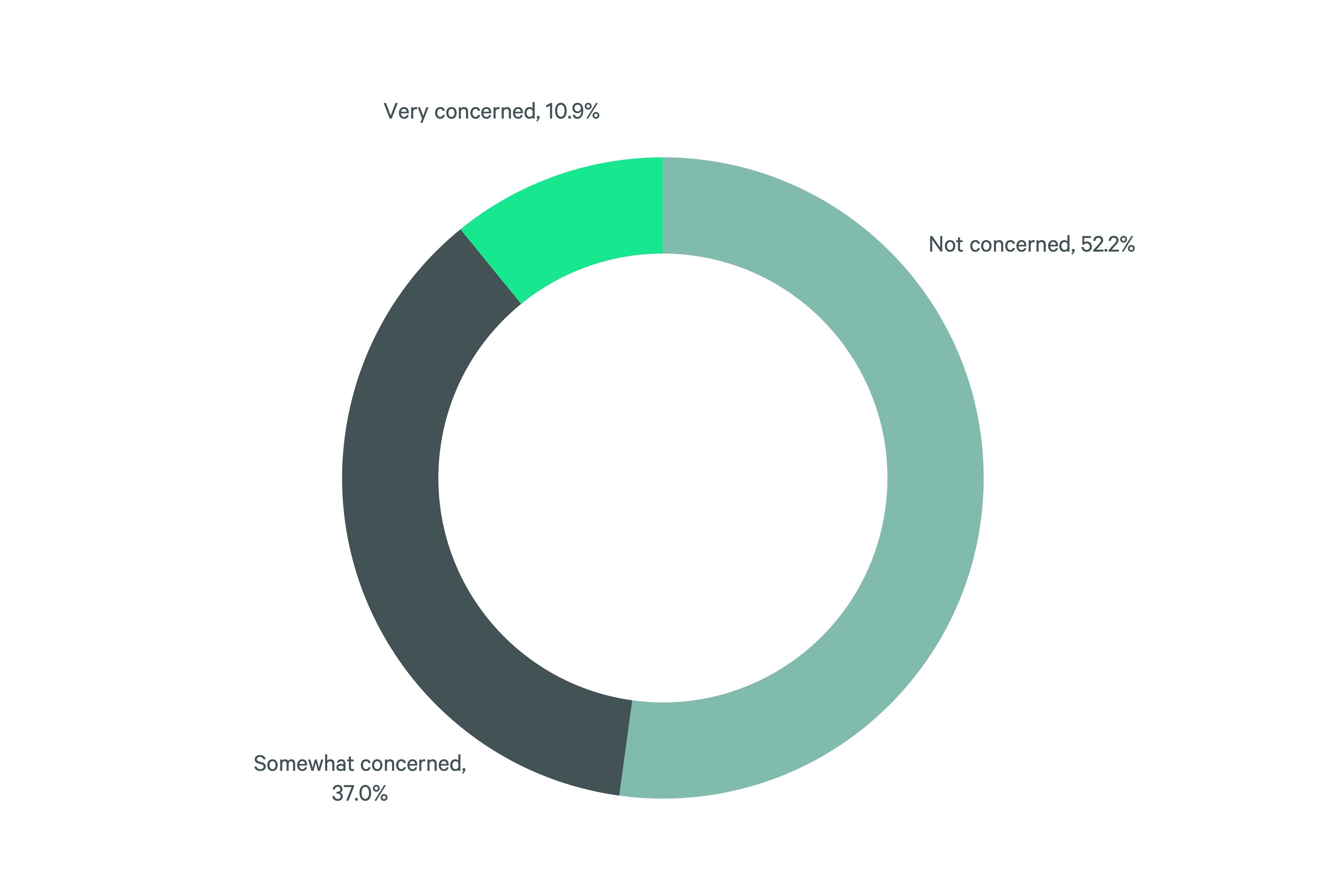

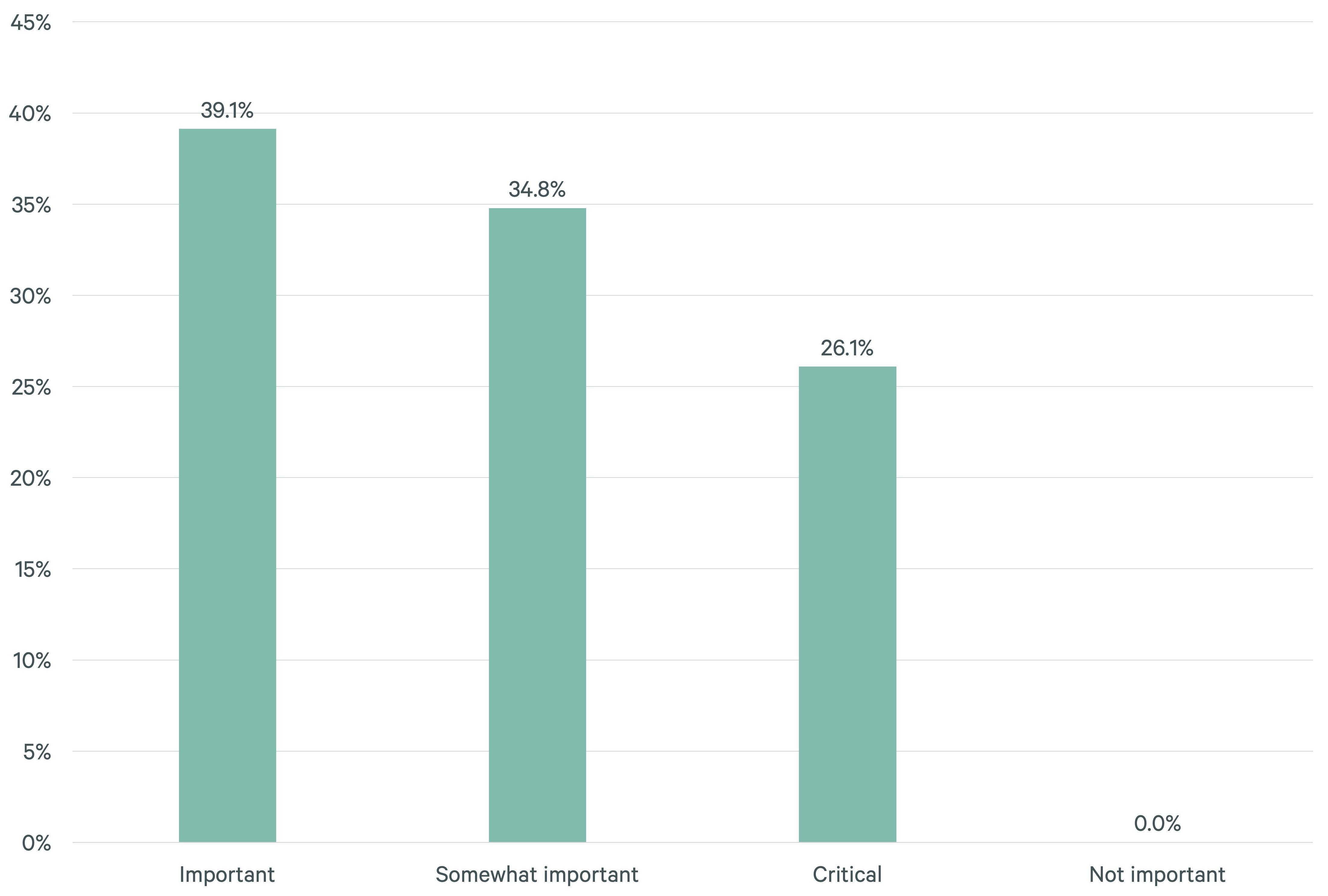

- Markets with nearby transportation hubs, including ports and major interstate highway access, are more highly valued than markets with reliable power grids. However, nearly 50%of respondents indicated that power availability and reliability was somewhat of a concern in target markets.

- Just over 40% of respondents said that trade policy would have no impact on their business operations this year. Only 11% said it would have significant impact. General retailers/wholesalers made up 60% of respondents who felt trade policy would have a significant impact.

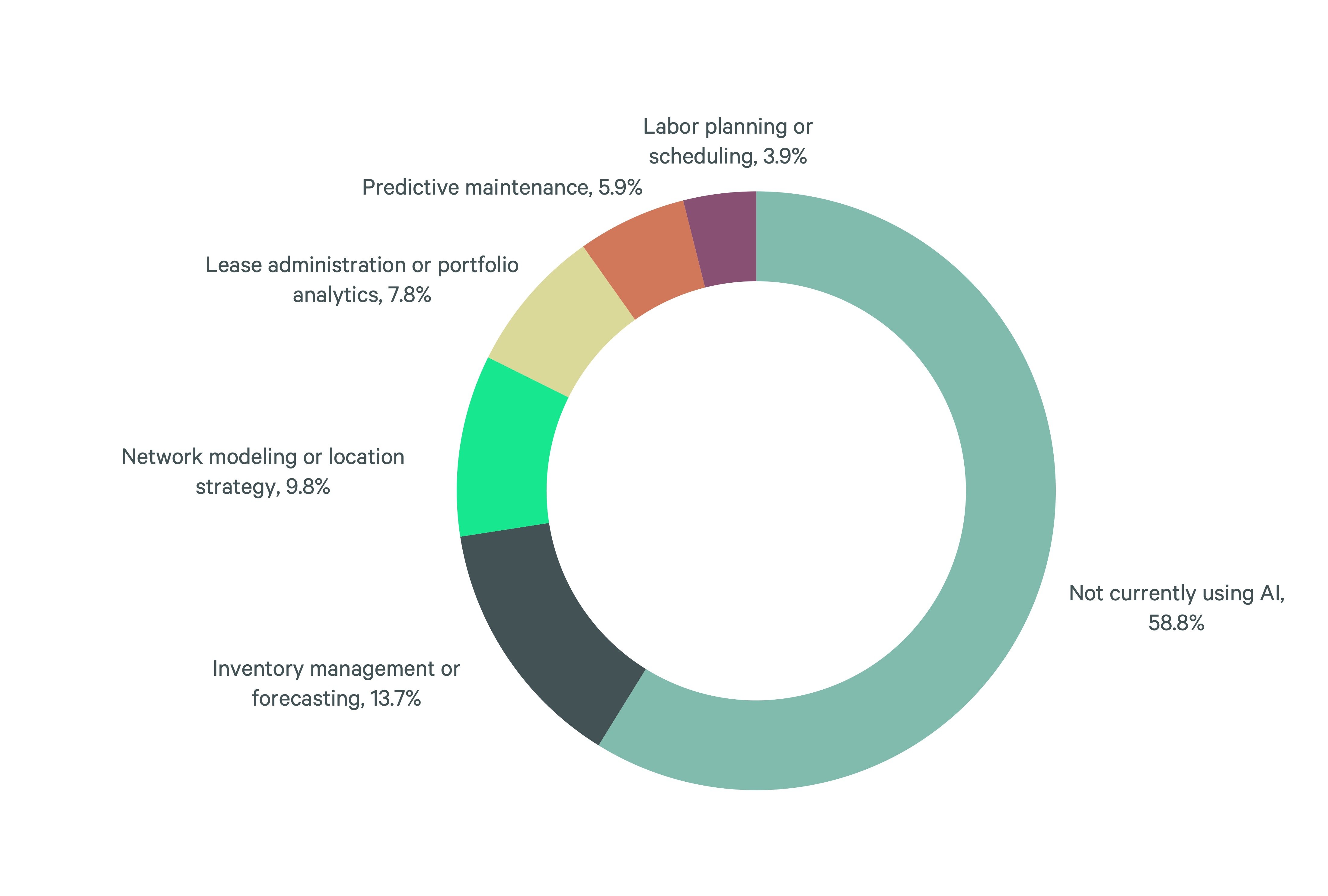

- AI does not appear to be a major concern for occupiers over the next 36 months. Fifty-nine percent of respondents are not currently using AI in their business and 36% are not planning to use it in the near future. For those that are already using AI or plan to do so in the near future, most are applying it to inventory management and location strategies.

Figure 11: What are your greatest business challenges today? (select up to 3)

Figure 12: What are the greatest real estate challenges facing your operations today? (select up to 3)

Figure 13: What are the main drivers for market site selection over the next 36 months? (select up to 3)

Figure 14: What are the most important building-selection factors when considering new facilities? (select up to 3)

Figure 15: How concerned are you with power availability and grid reliability in your target markets?

Figure 16: How important are nearby transportation connections (e.g., interstate highways, ports) to site selection?

Figure 17: To what degree do you expect U.S. trade policy to affect your operations in 2026?

Figure 18: How are you currently using AI to manage your portfolio or operations? (select up to 3)

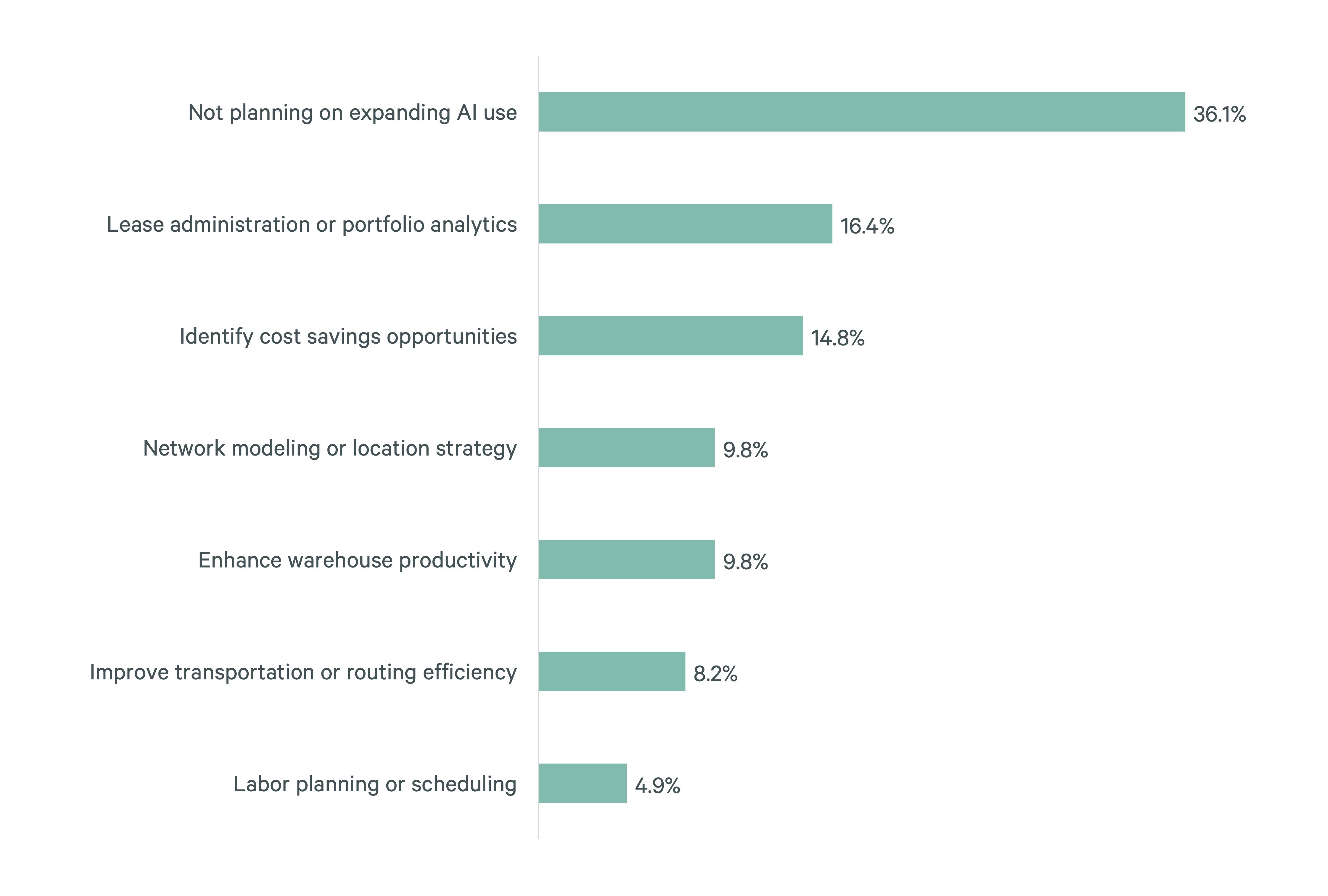

Figure 19: How would you like to use AI in the future to manage your portfolio or operations?

What It All Means

- The survey results generally correlate with CBRE’s outlook for the industrial market, which includes a flight to quality, greater use of 3PLs, a boost in domestic manufacturing and a greater focus on real estate costs.

- Investment opportunities include properties in the Southeast and Midwest regions that offer modern amenities and quick access to logistics hubs.

- Higher real estate costs, including rent, can eventually be a factor in consolidations by occupiers and lead to occupancy losses for building owners. Landlord concessions likely will be more prevalent for second-generation space in pre-2020 buildings.

- Power availability and AI are not top of mind for industrial occupiers today. While the survey does showcase some interest in future use of AI, the primary demand drivers remain location, labor and costs.

Related Insights

-

Brief | Adaptive Spaces

Shallow-Bay Industrial Availability Remains Tight Amid Strong Demand

March 24, 2026

Limited new development and strong demand from small occupiers keep shallow‑bay industrial vacancy low and rents rising across major U.S. markets.

-

Global capital is on the move. Explore how investor sentiment, sector priorities and strategy changes are reshaping real estate in 2026.

-

Brief | Intelligent Investment

Potential Impact of Rising Oil Prices on Real Estate Values

March 30, 2026

Oil price volatility impacts commercial real estate through inflation, interest rates, and occupier demand, affecting cap rates and investment returns.