Chapter 1

Economic Outlook

CBRE New Zealand Real Estate Market Outlook 2026

10 Minute Read

10 Minute Read

Looking for a PDF of this content?

Economic Outlook

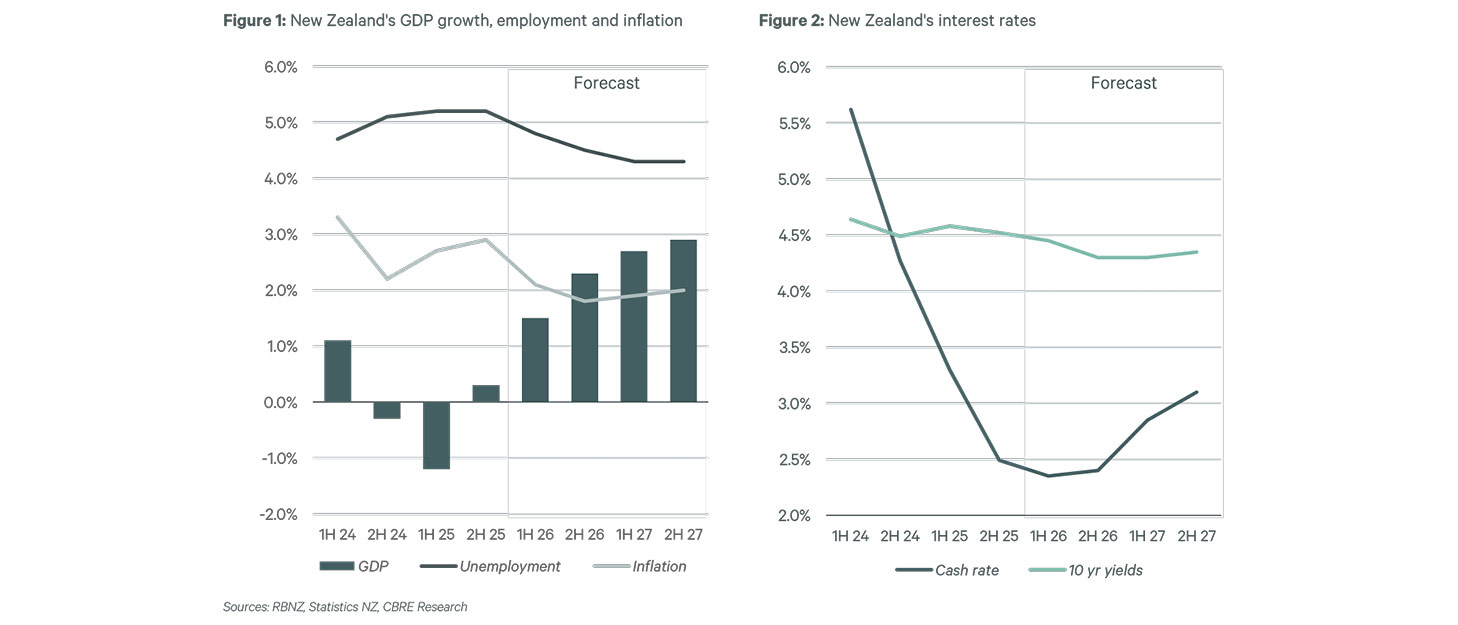

Sharp interest rate cuts are starting to flow through to higher activity. A rebound will be driven by a gradual improvement in private consumption and higher investment volumes. Exports are also expected to perform well, driven by favourable agricultural export prices.

For an in-depth understanding and comprehensive analysis, download the full report.

Sharp rate cuts starting to flow through to higher activity

While inflationary pressures persist, especially through government set prices, the economy’s spare capacity remains significant, giving the RBNZ some room to be growth-friendly for an extended period. This will likely lead the central bank to normalise monetary policy in 2027, although interest rate hikes may start late 2026.

Other central banks have eased by less than the RBNZ and are more cautious about how much capacity they have to cut, given inflation pressures. Whereas the OCR is 2.25% in New Zealand, the US Fed Funds rate is expected to remain above 3%. The contrast with Australia is even greater, with the RBA policy rate at 3.85% and unlikely to fall.

The resulting elevated bond yields in these countries is supporting New Zealand bond yields too. The consensus view is that long-ended interest rates have little room for further easing.

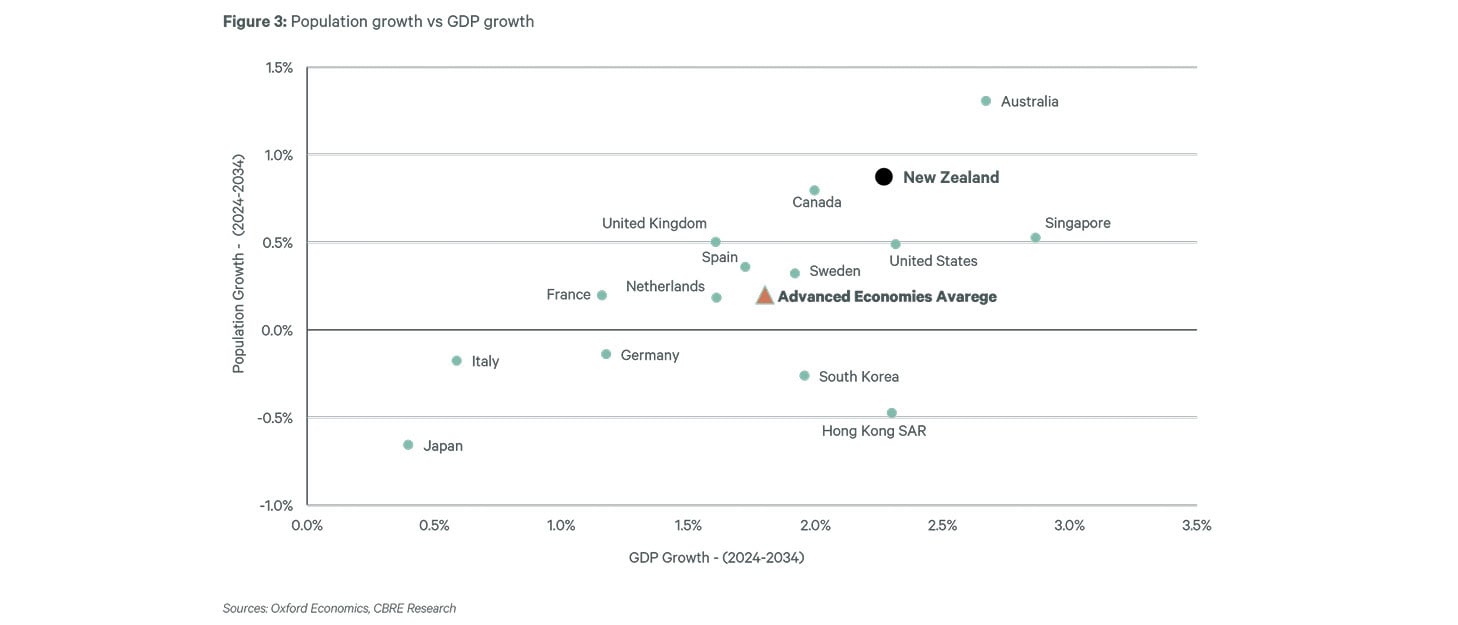

New Zealand’s population and GDP growth are projected to be above developed country averages

The population is forecast to increase by around 560,000 (11% growth) between 2024 to 2034. This is the equivalent to adding the population of Greater Christchurch (Christchurch City, Selwyn district and Waimakariri district), the second largest urban area in New Zealand.

In terms of GDP, New Zealand is among the group of countries expected to register an annual average growth rate around the mid 2.0% pa range in the next decade, above the developed world average. This will be driven by a gradual improvement in private consumption and higher investment volumes supported by lowered interest rates and growing confidence. Exports are also expected to perform well due to strong agricultural export prices. However, government spending is forecast to be muted in the next few years to achieve budget surpluses through strict fiscal discipline.

Cyclical and structural economic indicators show marked regional variations

However, in terms of unemployment, the South Island currently outperforms the North, with a rate of 3.5% compared to 5.3%. South Island regions have enjoyed lower unemployment rates due to a more dynamic economy in this cycle driven by a robust primary sector (helped by high commodity prices), a rebound in tourism and ongoing construction activity.

Where are the opportunities?

-

Rate cuts are beginning to stimulate economic activity

The 325 bp drop in the cash rate over the past 18 months is starting to feed into higher GDP growth, setting the stage for improving investment conditions as 2026 progresses.

-

Strengthening demand expected later in 2026

A material lift in occupier demand for business space is forecast for the second half of 2026, with a stronger absorption rebound expected to carry into 2027 and 2028.

-

Population growth will support long term real estate demand

New Zealand’s population is projected to increase by around 560,000 people between 2024 and 2034, one of the strongest growth outlooks in the developed world, underpinning sustained demand for space.

Related Insights

-

Report | Intelligent Investment

Pacific Real Estate Market Outlook - April 2026 edition

January 27, 2026

CBRE’s 2026 Pacific Market Outlook highlights key trends and overarching themes that will guide market shifts and decision making.

-

CBRE’s 2026 Asia Pacific Investor Intentions Survey uncovered a further improvement in buying intentions across most markets in Asia Pacific this year

-

The latest New Zealand Property Occupancy Costs and Rental Affordability report examines occupancy cost ratios and their implications for investors and occupiers. Read now.

-

In Q3, market yields experienced notable firming, the most significant since Q2 2021, as lower interest rates enhanced liquidity and pricing for assets.